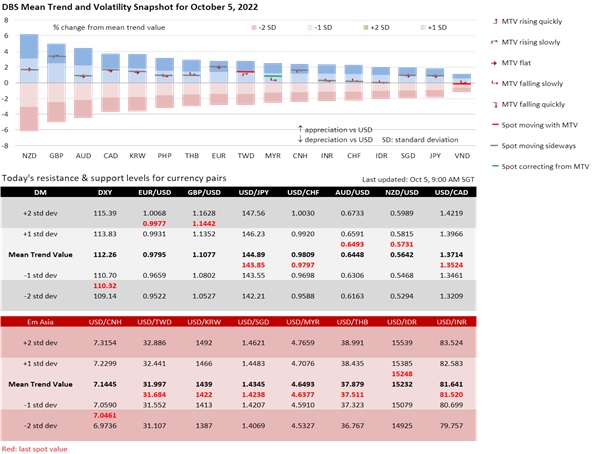

We are cautious about the USD’s sell-off at current levels. DXY depreciated from 114 to 110 in the past five sessions. The 14-day RSI is longer overbought above 80 and dropped to 46.7 on Tuesday. Markets were encouraged that the Fed might moderate the pace and magnitude of hikes. Apart from the Reserve Bank of Australia’s smaller 25 bps hike (vs 50 bps consensus), US JOLTS jobs opening slowed to 10.1 million in August from 11.2 million in July. The US Treasury 10Y yield eased 19 bps to 3.633%, while 2Y fell 2.1 bps to 4.093%. In turn, investors drove the Dow, S&P 500, and Nasdaq Composite higher by 2.8%, 3.1%, and 3.3%, respectively.

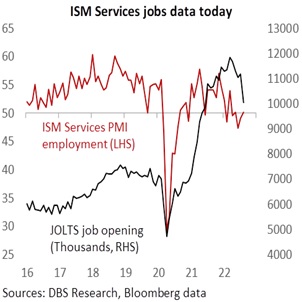

Fed officials will likely to push back against the market’s attempt to reinstate a less hawkish or dovish pivot. Speaking today, Fed Presidents Neel Kashkari (Minneapolis) and Raphael Bostic (Atlanta) will remind markets that the Fed’s job of controlling inflation is far from over. Consensus expects next week’s CPI and core inflation to hold above 8% YoY and 6% in September. Meanwhile, today’s ADP employment should improve to 200k in September from 132k In August, and Friday’s nonfarm payrolls to slow to 263k from 315k. Let’s see the employment index within the ISM Services PMI holds above 50 for a second month in September.

AUD depreciated 0.2% to 0.65, still consolidating between 0.6350 and 0.6550. The Reserve Bank of Australia delivered a smaller 25 bps hike to 2.6% yesterday after four 50 bps increases in as many months. With the cash rate target slightly above the 2.5% neutral level amidst a weaker economic outlook for 2023, the RBA will probably keep hiking by 25 bps in November and December. RBA still sees inflation rising to 7.75-8% early next year before slowing towards its 2-3% target range over the next couple of years. Fearing a global recession, Treasurer Jim Chalmers ruled out returning to a budget surplus over the next three years to the next election in 2025. Chalmers will present the Budget on 25 October after conferring with his counterparts at the G20 meetings of finance ministers and central bankers on 12 October. Meanwhile, AUD will take its cue from US equity futures, last signalling a weaker open in the US session.

Quote of the day

“We cannot hold a torch to light another’s path without brightening our own.”

Ben Sweetland

5 October in history

The first James Bond movie, Dr No, premiered in London in 1962.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.