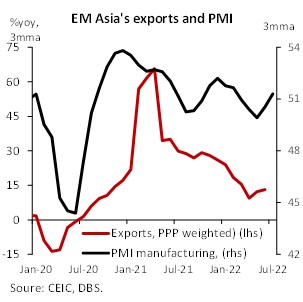

- Through June, aggregate exports out of Asia were up 13.1%yoy

- This outturn is impressive considering the adverse base effect in place

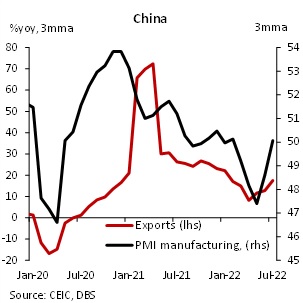

- July exports from China and South Korea were strong

- China’s burgeoning trade surplus also reflects weak domestic demand

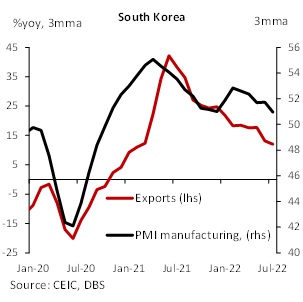

- South Korea’s auto exports have revived strongly, although semiconductor demand has softened

But so far, so good. Our measure of aggregate exports out of the region was up 13.1%yoy through June. The figure is even more promising for Asia ex-China (+20.6%yoy). On a chart, this may come across as a softening trend, but this outturn should be seen in the context of rather adverse base effects. At this time last year, on the back of a post-lockdown rebound, Asia’s exports were up 35%yoy, so a double-digit growth at the current juncture is indicative of sustained strength of the exports cycle. PMI manufacturing has stayed well above 50 lately, another source of comfort.

China

China’s domestic economy is facing multiple headwinds, including pandemic management struggles and a deepening property sector crisis, but through all this, the country’s factories have been humming, allowing the exporters to keep their operations going. The cost of shipping a container from Shanghai to Los Angeles has declined by over 40% since Q4 last year, suggesting that some of the supply side frictions related to ports have eased considerably, helping trade. China’s strong exports also reflect resilient demand from its largest importer, the US. With jobs and wages showing continued strength, American consumers have so far shrugged off the challenges posed by high cost of fuel and food, keeping retail sales growth in high single digits.

India

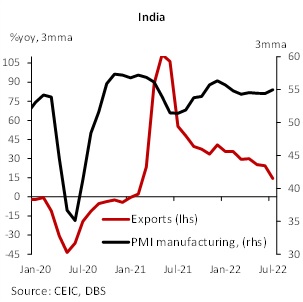

While China is running record trade surpluses, India’s trade deficit keeps widening (July deficit went past USD31bn). Exports demand has softened lately, while the high cost of energy imports has kept the import bill elevated. A recent contraction in the export of refined fuel may be attributed to the government’s levy of windfall tax on oil exports, which is being calibrated and the impact may turn out to be temporary. PMI surveys post a favourable picture, with manufacturers holding their own despite rising costs and RBI rate hikes.

On the back of strong demand from both the US and EU, South Korea’s July exports crossed USD60bn, up 9.4%yoy. Auto exports have recovered robustly after last year’s chip-shortage led disruptions. Semiconductor demand, however, has begun to weaken, just as supply has caught up.

Asia’s exports have therefore begun the second half of the year still in good shape. Chances are the going may get tough as demand in US, EU, and China soften further, but it is heartening to see that export earnings have not yet been hit as much as we had feared given the plethora of outstanding headwinds.

To read the full report, click here to Download the PDF.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.