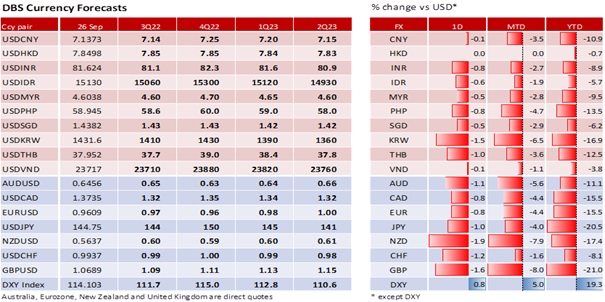

GBP overtook JPY as the weakest DXY currency this year. GBP depreciated 21% YTD vs 20.5% in the JPY. On Monday, GBP fell 1.6% to 1.0689, not before plunging 4.7% to a new lifetime low of 1.0350 at the start of the Asian trading session. The previous all-time low was 1.0520 in February 1985. During the European session, GBP rebounded 1.0931 on expectations for the Bank of England to jack up rates to stabilize the currency. However, the recovery subsided after the BOE issued a statement that it would only act after thoroughly assessing the impact of fiscal plans and the GBP’s weakness on inflation at the next monetary policy committee meeting on 3 November. GBP is not out of the woods yet. Another rise in Gilt yields and option volatility might send it lower again.

The collapse of the GBP and the spike in Gilt yields reflected the market’s unwillingness to endorse the tax cut plan announced in the mini-budget last week. The National Institute of Economic and Social Research (NIESR) estimated the Truss government’s borrowing-to-spend plan would widen the budget deficit to 8% of GDP this financial year. Bloomberg consensus projects a current account deficit of 5.6% of GDP in 2022, wider than the 5.3% in 2016, the year of the Brexit Referendum. Last Thursday, the BOE raised rates by 50 bps, clear about its priority to rein in elevated inflation even as it predicted the UK economy entering a technical recession in 3Q22. The Office for National Statistics is scheduled to release the 3Q22 GDP report on 30 September. Former US Treasury Secretary Lawrence Summers warned that the UK was behaving a bit like an emerging market, pursuing the worst macroeconomic policies of any major country in a long time that threaten to sink GBP below parity against the USD.

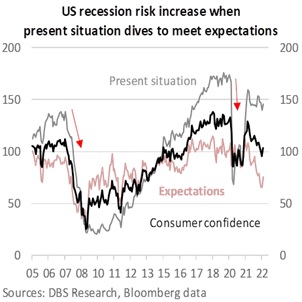

In the overnight markets, the Dow, S&P 500 and Nasdaq Composite fell 1.1%, 1.0% and 0.6% respectively. Atlanta Fed President warned that UK’s fiscal path could heighten volatility in global financial markets and hurt the global economy. Boston Fed President Susan Collins warned that external shocks like a significant economic or geopolitical event could push the US economy into recession. Today, the US Conference Board’s consumer confidence index might disappoint. Consensus expects headline confidence to improve to 104.5 in September from 103.2 in August. However, nonfarm payrolls did slow amidst a rise in the unemployment rate earlier this month. Today’s new home sales might also dip below 500k (consensus) in August. The Fed’s aggressive stance to control inflation at the expense of growth and jobs should turn the American consumer cautious too. Hence, pay close attention to the present situation index for signs of weakness. After two days of strong appreciation, DXY might consolidate inside its new 110-115 range.

Quote of the day

“Whoever is careless with truth in small matters cannot be trusted with important matters.”

Albert Einstein

27 September in history

The Republic of China was recognized by the United States in 1928.

Subscribe here to receive our economics & macro strategy materials.

To unsubscribe, please click here.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.