In investment financing, you borrow money from a bank to invest. That loan is secured by your bank-managed assets acting as collateral, which may include deposits, stocks, bonds, funds, and other investment assets.

In assessing whether an asset is a suitable collateral, we consider:

How easy is it to convert the asset into cash?

How volatile is the asset’s market value?

For bonds, what is the credit rating, or where there is no credit rating, the issuer’s financial strength?

Taking into account these factors, we derive the loanable value, or percentage of market value against which we lend you. The asset’s collateral value is then obtained by multiplying its market value with its loanable value.

The collateral value must always be equal to or more than the loan amount.

Example:

Let’s say you believe Bond A presents an attractive investment opportunity. You have $1,000,000 in cash to buy Bond A. With a financing amount of $1,500,000, you can invest $2,500,000.

With a 60% loanable value, the collateral value of the bonds bought is: $2,500,000 x 60% = $1,500,000

This exactly covers the loan amount.

For illustration purposes only.

In the event the collateral value falls short, you will need to either:

Raise the collateral value by:

Or

Reduce your loan exposure by:

Investment financing may carry significant risks and is not suitable for investors who do not comprehend it or are risk-averse.

Investment financing can enable you to invest more capital than you have on hand — and potentially increase your investment return. This is also known as “leveraging” or “gearing”.

However, do note that leverage is a double-edged sword. If the investments rise in value, your returns are magnified. But if the investments move adversely, your losses will also be amplified.

Here are some examples of how borrowing to invest can add value to your investment strategy.

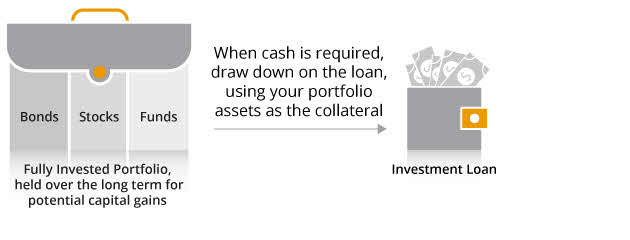

1. Fully invest your portfolio, while enjoying liquidity when you need it

Holding cash in your investment portfolio to meet short-term liquidity needs.

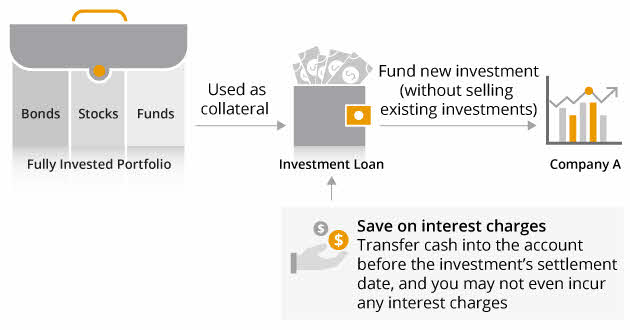

2. Acting on investment opportunities quickly

You have a fully invested portfolio. An investment opportunity in Company A arises, and you want to act quickly — but without selling existing investments to fund the purchase. Transferring funds from another bank may be too late.

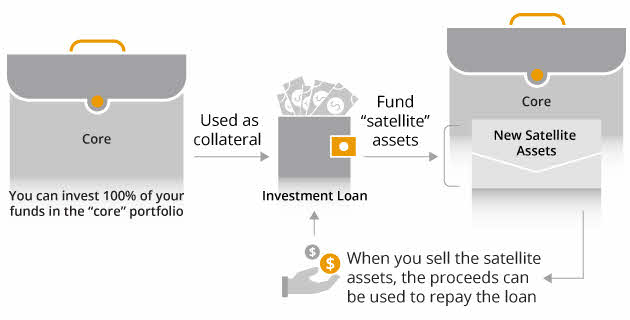

3. Implement a core-satellite investment approach

You wish to implement a core-satellite approach, in which the “core” portfolio comprises globally diversified assets to be held over the long term, while the “satellite” portfolio is made up of short- to medium-term investments for tactical gains.

4. Leverage your investments

You wish to invest more than you have, and can withstand the potential risks of gearing.

You can invest more capital than you have on hand. Please see example in “How Leverage Works”.

Disclaimer for Investment Products.

Credit Facilities Terms and Conditions apply.

or your Relationship Manager for more information.

To draw down loan on DBS digibank.

Phone - 1800 221 1111

Have someone contact you

Help & Support Portal

Feedback