Key points:

- Legacy planning is about passing your assets to the ones you care about. It is an expression of what you value and what you want your legacy (or your home) to reflect.

- Apart from material wealth, you can also pass on intangible gifts, such as imparting certain values to enrich the lives of your loved ones, or establishing charitable giving.

- Without a legacy plan in place, your family members and business partners might end up spending a lot of time and resources trying to sort out the distribution of your assets.

- A good legacy plan allocates your assets meaningfully while maintaining harmony between your loved ones. A robust plan considers the associated complexities and explores all the options available to you.

Keen to add robustness to your legacy plan?

Like many other high-income earners, you might be preparing the next generation for wealth by solidifying your legacy planning.

Talking about wealth transfers can be a tricky subject to broach. According to a 2019 Asia Private Banker report, the main hurdles faced by Asia’s high net worth individuals (HWNIs) are procrastination and the perceived complexity of the process1.

Think of legacy planning and wealth transfers as similar to the process of planning and designing your dream home. You get to decide what you want to do with your space, plan and select the décor, and allocate resources to it. Without effective space planning and interior decor, your home can lack a cohesive sense of form and function that makes them attractive and usable to you. In the same way, there are pitfalls if you neglect legacy planning too.

What happens if we don’t talk to our families about legacy planning? And how can you as a modern affluent tackle the topic of wealth transfers?

What is legacy planning?

Legacy planning is about passing your assets to the people you care about. Drawing a parallel to designing your home, both are an expression of what you value and what you want your legacy (or your home) to reflect.

Legacy planning is about deciding how exactly you'd like your assets distributed to your loved ones. Apart from material wealth, you can also pass on intangible gifts, such as imparting certain values to enrich the lives of your loved ones, or establishing charitable giving.

Similarly for your home designing, you would decide what you want in each space — If you have children, their rooms, study and play areas would be an important focus. Or if you enjoy cooking, putting more emphasis on the kitchen would be one of your priorities. The planning of both your legacy and your home is essential to ultimately create what you want.

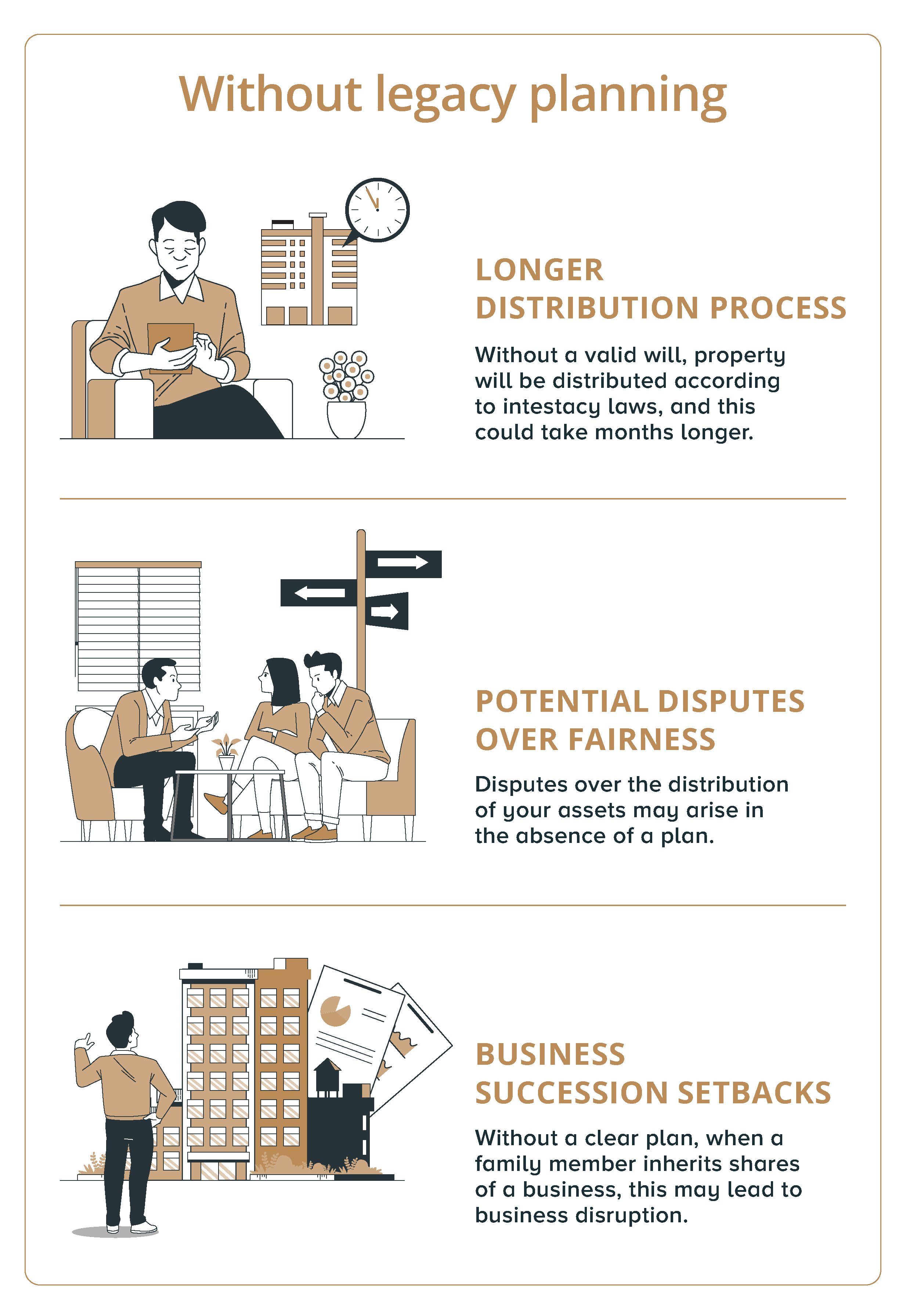

What happens without legacy planning?

Without a legacy plan in place, your family members and business partners might end up spending a lot of time and resources trying to sort out the distribution of your assets.

Longer distribution process

Without legacy planning, your assets will be distributed according to Singapore’s Intestate Succession Act. For Muslims, the Islamic inheritance law will apply. The process could take months longer, with outcomes that aren’t aligned with your wishes.

(Read more: What successful legacy planning looks like in Singapore)

Potential disputes over fairness

Even with legacy planning in place, family members have reportedly tussled over the ownership of assets, and guardianship of the surviving children.

That’s why, even more so, not having a plan in place could lead to disputes over fairness, especially if a large proportion of assets cannot be easily converted into cash — For instance, if the bulk of your wealth is in real estate, antiques, art or businesses. Distributing your estate equally is difficult as each asset has a different value.

Business succession setbacks

For business owners, the business could make up a large part of your net worth, which you want to use to support your loved ones.

When a business owner passes on, their family inherit their share of the business. This may lead to business disruption as the family members may not have experience or knowledge about running the business.

One solution is for the other shareholders to buy over your share of the business, but the subsequent challenge will be in agreeing how much these shares are worth.

The value of successful legacy planning

Meaningful legacy planning gives purpose to the wealth and assets you created. Like a well-planned and meaningfully designed home, it forges lasting connections for your loved ones and gives them a common ground to live and progress.

Conscientious legacy planning takes into account asset liquidity, coverage for liabilities, fair distribution and diversification to offset any changes.

Estate liquidity to cover liabilities

It’s common to have assets that are not easily converted into cash, such as businesses, real estate, antiques, and art.

With life insurance as part of a sound legacy plan, your family can rely on the liquidity of payouts, instead of being forced to sell these illiquid assets to cover large medical bills or unpaid debts.

Estate equalisation for fairer distribution of assets

Estate equalisation is useful when some of your assets are illiquid; By having other assets such as whole life insurance and universal life insurance that offer payouts, you can distribute equal value of assets to your beneficiaries.

The estate equalisation strategy is employed where one asset (for instance your business) is distributed to one beneficiary, and other assets of an equivalent value (insurance payouts) is given to another. This also helps to mitigate jurisdictional, compliance, legal, and tax issues.

Portfolio Diversification

Investment markets can be volatile and lead to large fluctuations in returns. If a large part of your assets is in higher risk assets, this could affect the value your legacy. In contrast, life insurance are lower risk assets which allow you to receive returns, while protecting you from market fluctuations.

Including life insurance in your portfolio of investments and businesses ensures there’s sufficient assets to distribute to your family.

For instance, single-premium plans such as Signature Income Series and Signature Lifetime Rewards provide a reliable stream of returns.

And universal life insurance products such as Heirloom (IV) and Signature Indexed Universal Life (II) can pay a lump sum to your legacy.

Create a meaningful family legacy

Like creating your dream home for your family, at the heart of legacy planning is allocating your assets meaningfully while maintaining harmony between your loved ones. A robust plan considers the associated complexities and explores all the options available to you.

At DBS Treasures, your relationship manager can access intelligent wealth management tools to better identify your needs and develop a meaningful legacy plan that works for you.

Protect your loved ones and enhance the value of the legacy you built with our legacy planning solutions today.