Frequently Asked Questions

To ensure your SRS contribution is correctly reported to IRAS, please visit the nearest DBS or POSB branch to update your tax reference number of your SRS Account.

At the Branch, please ensure you

- Bring along your relevant original copy of the identification documents for verification

- For Singaporeans/Permanent Residents

- Provide NRIC.

- For Foreigners

- Identification Document:

- Provide Passport

- For Malaysian – Valid Malaysian IC

- Proof of Employment (if you are working in Singapore)

- Valid Employment pass / In Principal Approval (IPA) issued by Ministry of Manpower (to update your Foreign Identification Number)

- Identification Document:

- Update your tax reference number (e.g. NRIC/FIN) of your SRS Account in the Bank’s record.

You can do so via digibank or at the branch. For contribution via digibank, simply perform a funds transfer to your SRS Account. Please visit this page for more information on contribution channels and deadlines.

You do not need to make a claim in your tax return as it will be allowed automatically based on information provided by us to IRAS.

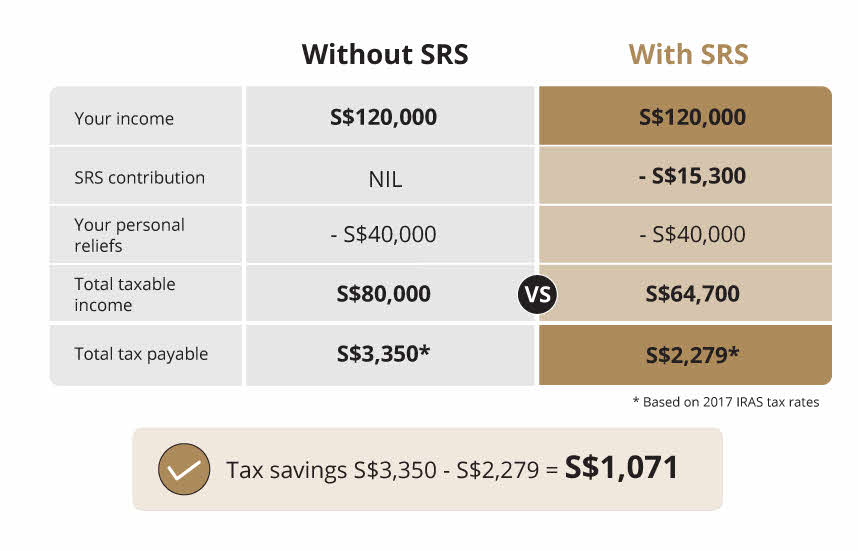

The yearly contribution for a Singaporean or Singapore Permanent Resident is capped at S$15,300. If you're a foreigner, you'll be allowed a higher yearly contribution of S$35,700 as you do not enjoy tax relief on your CPF contributions.

For Foreigners, please declare your Foreigner status at the branch to update your SRS contribution cap for the year. (Note: This declaration needs to be done yearly as the SRS contribution limit will reset on 1 January each year)

If you become a Singapore Citizen or Singapore Permanent Resident during the year, please update the SRS operator as your maximum contribution amount will have to be recalculated even if you have already made contributions for that year. The bank will re-compute your SRS contribution cap for the year on a pro-rata basis.

Penalties may be imposed for excess contributions if a wrongful declaration has been made to the SRS operator.

For foreigners, please declare your Foreigner status to update your SRS contribution cap for the year yearly2.

- Update instantly via digibot

Launch digibot

- Visit the branch

Please ensure you bring along your relevant original copy of the identification documents for verification at any Branch or Financial Planning Branch. Find your nearest branch.

- Identification Document:

- Valid Passport

- For Malaysian - Valid Malaysian IC

- Proof of Employment (if you are working in Singapore)

- Valid Employment pass / In Principal Approval (IPA) issued by Ministry of Manpower (to update your Foreign Identification Number)

2 Please note that your SRS contribution limit will reset on 1st Jan every year.

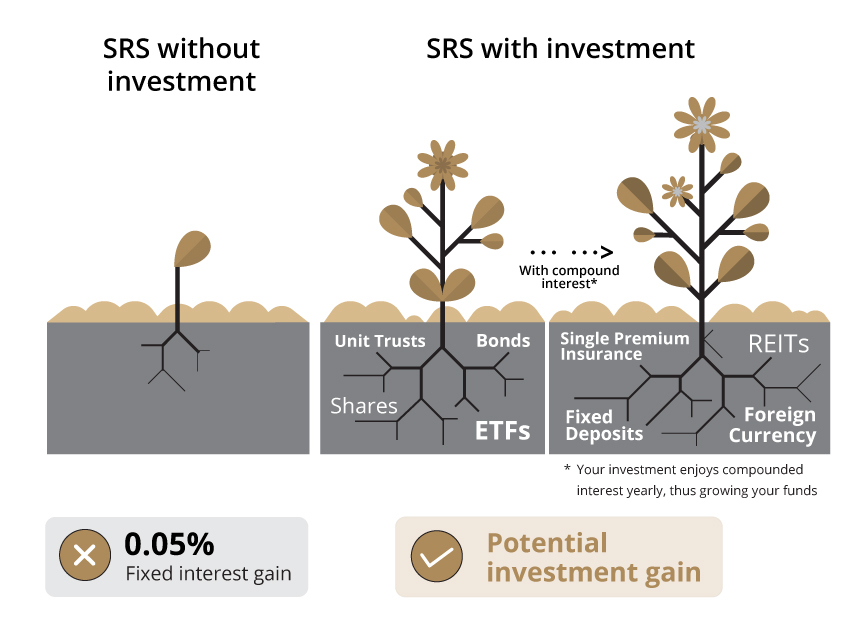

Yes, you can speak to us on how you can maximise your SRS funds.

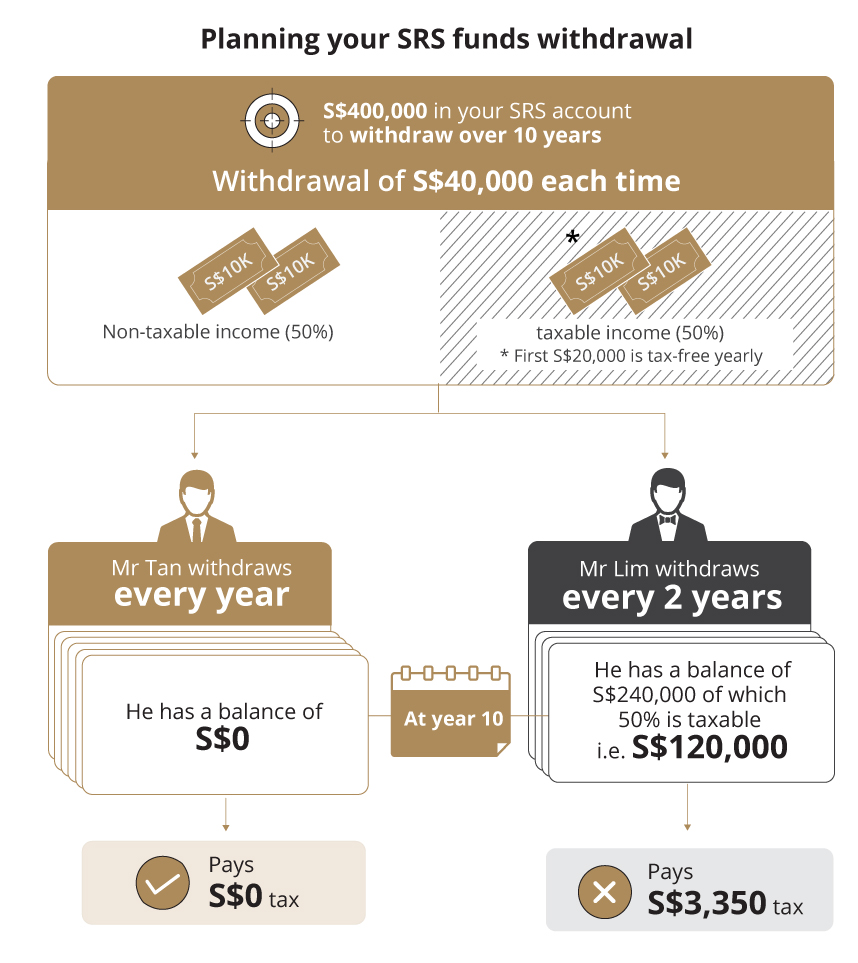

You can withdraw from your DBS SRS Account at any time before retirement age at first contribution, subjected to a 5% penalty for early withdrawal. 100% of the amount withdrawn will also be subjected to tax for that year.

Regardless if you are doing an early or penalty-free withdrawal, please visit any DBS/POSB Branch to process your SRS withdrawal.

Login to digibank and easily view the following information on your SRS Account:

- Maximum contribution amount

- Total contribution made to date

- Balance contribution limit

- Cash balance

You can only have one SRS account at any point in time. It is an offence to open SRS Accounts with more than one operator and there are penalties for doing so.

Instead, if you have an existing SRS Account with another SRS operator and wish to transfer to DBS, please visit any of our branches to do a SRS Account transfer.

You can visit any of our branches to complete and sign the following forms:

- SRS Account Transfer form

- SRS Account Application form

- SRS Annual Declaration form (Applicable to foreigners only)

The standard time frame to complete the inter-bank transfer process is 7 working days.

Effective 10 Dec 2018, the settlement cycle for securities is two days (Trade date plus two days) to align with the new SGX securities settlement cycle. Please ensure that you have sufficient cash and securities balance in your SRS account before requesting for any securities transaction with us. Your trade will be accepted up to your available funds or securities upon receipt by the bank.

Information on shares corporate action event, can be found in the SGX website. Refer to Company Announcements, under Company Information.

The "security credit date" information can be found in the SGX website. Refer to Company Announcements, under Company Information.

The bank will charge a transaction fee of $2 for each Singapore Savings Bond application and redemption request. Otherwise, all SRS account transaction charges are waived until further notice.

Note: Third-party related charges such as CDP administrative fees and sales charges when investing using your SRS funds will still apply. Please check with the product provider you are investing with for the relevant fees and charges.