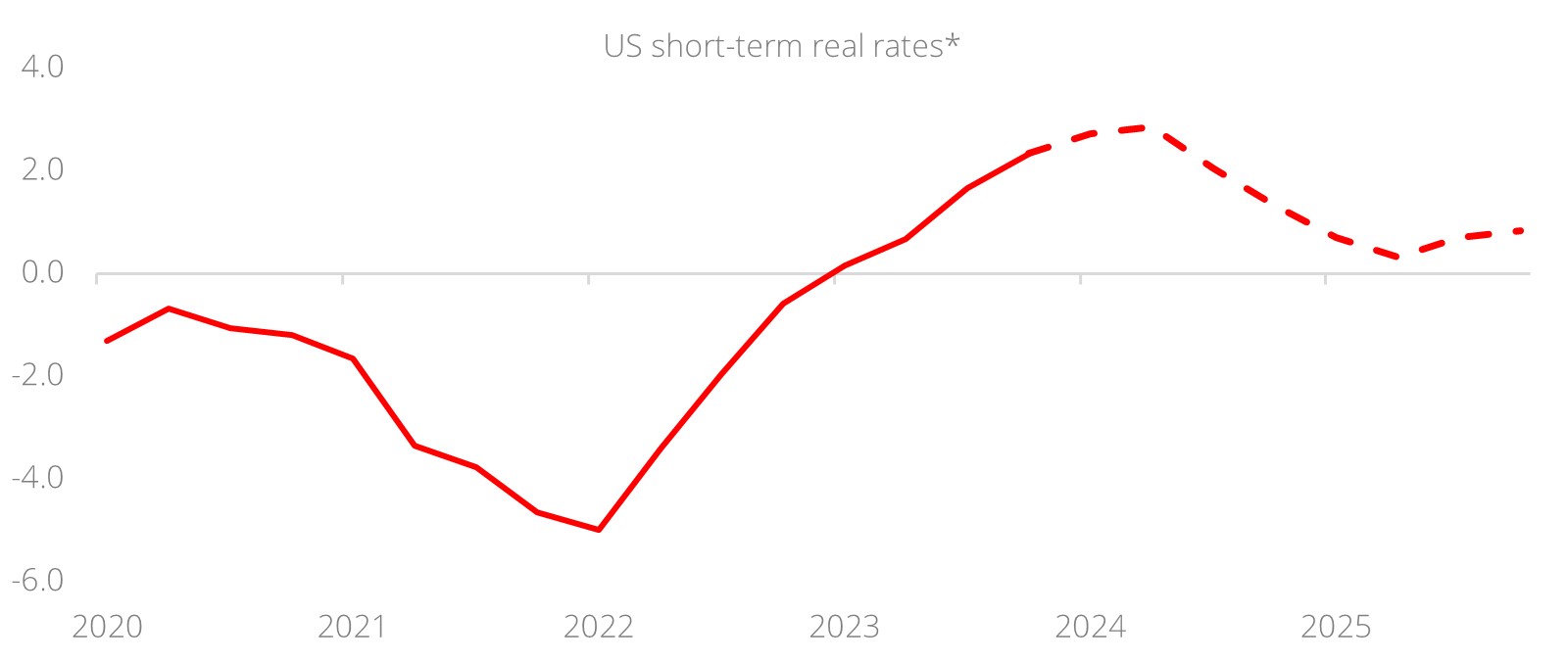

- US: Fed reaffirms focus on rate cut trajectory; 2Q24 will mark the peak in US short-term real rates

- Singapore: Steady MAS policy in upcoming Apr review; lower inflation forecast ahead

- Thailand: Worst is likely over following the late-Mar approval of the delayed FY2024 budget

- Vietnam: On track for gradual growth recovery driven by uptick in export-oriented activity

- Inflation and Growth Concerns Deepen26 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- Fed Cut Hopes Fade on Sticky Inflation12 Apr 2024

US: Fed sticks to cautious rate cut strategy. In line with expectations, Fed Chair Jerome Powell affirmed this week that the Fed would reduce the restriction in monetary policy weighing on aggregate demand once it was confident that inflation was on a sustainable path to the 2% target. He noted that accelerated immigration and increased prime-age participation brought a better balance between labour supply and demand.

Prices paid fell a second month to 53.4 from 58.6, its lowest level since March 2020, suggesting negative surprises for next week’s US Consumer Price Index inflation. Services employment increased from 48 in February to 48.5 in March, less than the 49 consensus and below the breakeven 50 level for a second month. Today (5 Apr), markets are bracing for nonfarm payrolls to fall to 213k in March from 275k in February.

According to a US Treasury press release, US Treasury Secretary Janet Yellen will visit China on a diplomatic trip to manage their bilateral economic relationship, and advance American interests. Yellen will likely follow up on China’s “unfair trade practices and non-economic practices,” an issue US President Joe Biden raised during his call with China President Xi Jinping earlier this week and seek more insights on China’s economy.

Peak in US short-term rates. We believe 2Q24 will mark the peak in US short-term real interest rates, defined as the difference between Fed Funds rates and core PCE inflation. Fed policy rate cuts are on the cards from mid-year onward even if core inflation does not ease much more. However, we do not expect negative real rates in this cycle as room for rate cuts through 2024/25 may well be limited by some stickiness in inflation and resilient demand.

Figure 1: 2Q24 should mark peak in US short-term rates

Source: CEIC, DBS

* Short-term real rates calculated by taking the difference between end-quarter Fed Funds rate and the average core PCE inflation for that quarter

Download the PDF to read the full report which includes insights on Singapore, Thailand, and Vietnam.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

- Inflation and Growth Concerns Deepen26 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- Fed Cut Hopes Fade on Sticky Inflation12 Apr 2024

- Inflation and Growth Concerns Deepen26 Apr 2024

- Central Banks Hold Steady19 Apr 2024

- Fed Cut Hopes Fade on Sticky Inflation12 Apr 2024