The European Central Bank meeting on April 11 presented a potential “buy the rumour, sell the event” scenario for the EUR. EUR/USD tested 1.07 amid speculation that the ECB might lower interest rates ahead of the Fed. While a few governing council members favoured a cut yesterday, the majority opted to wait until June, seeking more information to confirm that inflation was on track to the 2% target in a sustained and timely manner. Until the next ECB staff projection in June, ECB President Christine Lagarde adhered to the current assessment for inflation to average 2.3% in 2024 before declining to target in 2025. In line with our expectations, the ECB statement did not pre-commit to a particular rate path.

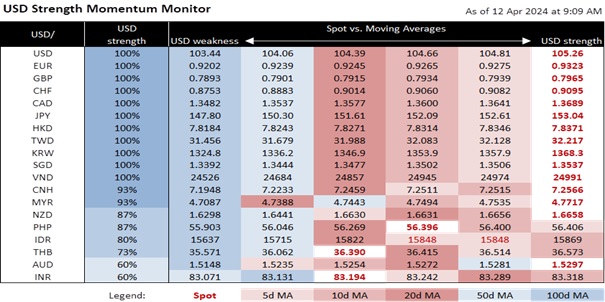

DXY was little changed at 105.28 on Thursday despite a brief spike to 105.53. New York Fed President John Williams’ comments suggested that markets might have overreacted to the sticky US CPI inflation. Williams reminded markets that the Fed’s preferred inflation gauge was the PCE deflator, which was well off its 40-year peak of 7.1% YoY in June 2022 to 2.5% in February. Williams believed the Fed could start lowering interest rates in 2024 despite his expectation for PCE inflation to fluctuate around 2.25-2.50% this year before moving closer to the 2% target in 2025. He also observed that inflation expectations had reverted to the Covid lows. The 1Y inflation expectations gauges by the New York Fed and the University of Michigan had fallen to late 2020 levels. Today. San Francisco Fed President Mary Daly will likely concur with Williams that there was no urgency to adjust policy at the upcoming FOMC meeting on May 1. Daly was probably among the ten out of 19 members who voted for three cuts this year.

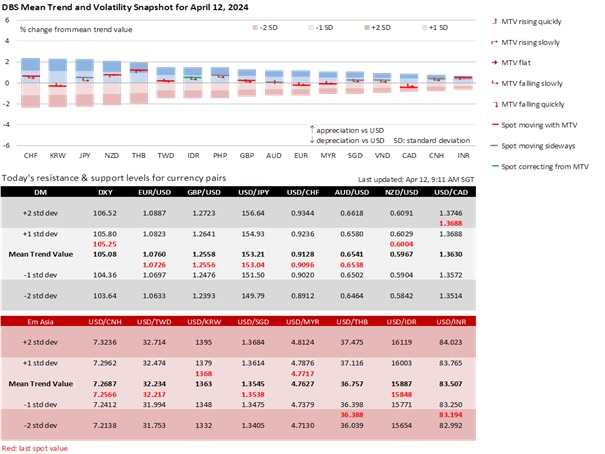

In line with our expectations, the Monetary Authority of Singapore did not adjust any of the three parameters of its SGD NEER policy band. MAS maintained the forecast for CPI-All Items inflation and its core inflation to average 2.5-3.5% in 2024, excluding the impact of the GST increase to 1.5-2.5%. Mirroring the trend in many countries, MAS reckoned core inflation will stay elevated earlier in the year. However, it maintained the stance for core inflation to moderate and step down in 4Q24 before falling further in 2025. Meanwhile, advanced GDP growth rose to 2.7% YoY in 1Q24 from 2.2% in 4Q23 but decelerated to 0.1% QoQ sa from 1.2%. MAS anticipated that the Singapore economy would strengthen over 2024, with growth becoming more broad-based, supported by an upturn in the electronics cycle and an anticipated easing in global interest rates. The Ministry of Trade and Industry maintained its forecast for the economy to expand by 1-3% in 2024. We maintain our forecast for the central bank to slightly reduce the slope of the SGD NEER policy band at the July meeting.

Quote of the day

"Patience is bitter, but its fruit is sweet.”

Jean-Jacques Rousseau

12 April in history

The Union Jack was adopted as the national flag of Great Britain in 1606.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.