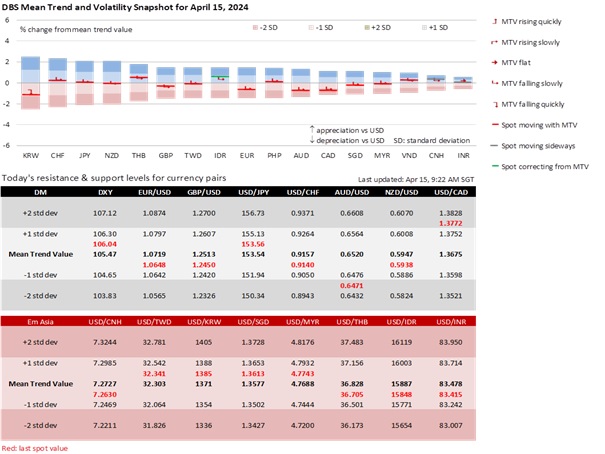

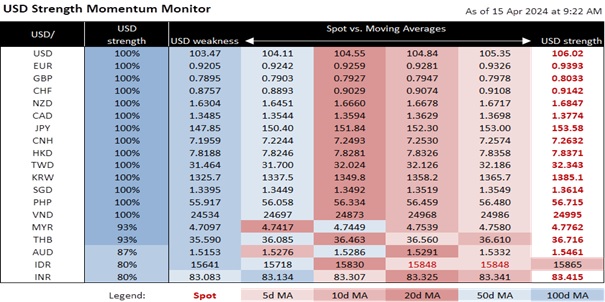

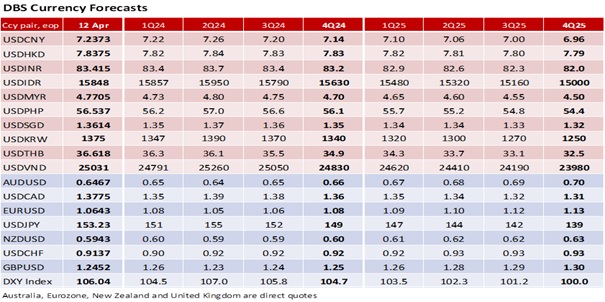

We have revised our currency forecasts favouring the USD’s recovery, extending from 1Q into 2Q 2024. Due to sticky inflation and a tight labour market in the US, we now see the Federal Reserve lowering interest rates by 50 bps instead of 100 bps in 2H24. Between 4Q and 3Q 2023, the monthly average for US nonfarm payrolls increased to 276k from 212k, while CPI core inflation firmed to 0.4% MoM from 0.3%. Assuming the PCE deflator on April 26 mirrors the CPI, fewer Fed officials will back the base scenario of three rate cuts this year before next week’s blackout period. On March 20, nine of the 19 Fed officials predicted two or fewer cuts in the dot plot. Hence, we cannot rule out the Fed reducing its projection from three to two rate cuts in June.

That said, history has demonstrated that when the US inflation gauges, especially the PCE deflators, resume their downward path towards the 2% target amid a gradual rise in the unemployment rate, the Fed will turn dovish again. Hence, we have maintained the profile for the greenback to depreciate after 2Q24 based on our forecast for the Fed to lower rates every quarter from 3Q24 through 2025. We do not rule out the first reduction taking place earlier in July vs. the September cut discounted by the interest rate futures. To do so, the next monthly US jobs and inflation reports will need to disappoint for the Fed to prepare for such a move at the June meeting.

Meanwhile, IMF Managing Director Kristalina Georgieva cautioned central banks against easing policy too early and risk a resurgence in inflation and a fresh bout of tightening. Hence, we expect more volatility from other central banks tempering their rate cut guidance, wary that markets are keen to see who would lower rates before the Fed.

Last week, the Bank of Canada warned that lowering rates too soon could jeopardize the progress to bring inflation to target despite not wanting rates to stay this restrictive longer than needed. Having noted that other central banks were cautious about easing monetary policy, the Reserve Bank of New Zealand wanted to keep its official cash rate restrictive for a sustained period to return CPI to target this year. Although the Reserve Bank of Australia shifted from a tightening to a neutral bias, it did not rule “anything in or out” on rates. The European Central Bank was unwilling to pre-commit beyond the rate cut expected on June 12, a decision that still hinges on the next two monthly inflation readings maintaining its downward trajectory.

Global central banks and financial markets will pay close attention to the impact on oil prices from the latest escalation in the tit-for-tat attacks between Israel and Iran. After bottoming at USD72.30 per barrel in mid-December, crude prices surged 25% to USD90 in April. Iran fired hundreds of drones and missiles in response to the attack on its Syrian embassy on April 1, its first direct attack on Israel after decades of shadow war. The US, the UK, and France helped to intercept the missiles. Turkey, Kuwait, and Qatar refused the US to use their airspace for retaliatory attacks on Iran. The United Nations warned that the Middle East was on the brink of a wider war.

Quote of the day

"Peace is not the absence of conflict, it is the ability to handle conflict by peaceful means.”

Ronald Reagan

15 April in history

The Titanic sank in 1912 after striking an iceberg on its maiden voyage.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.