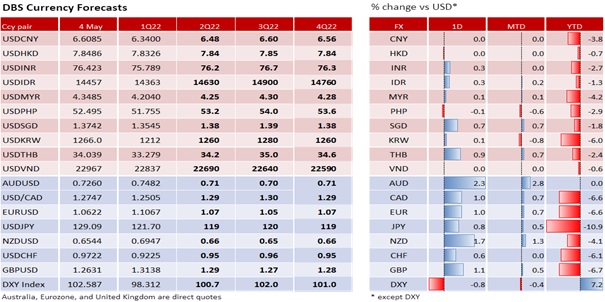

In line with our expectations, the FOMC meeting turned out to be a “buy the rumour, sell the fact” event for the USD. DXY depreciated 0.9% to 102.51, its lowest level since 26 April. The US Treasury 2Y yield fell 14 bps to 2.642% after the Fed delivered the well-telegraphed 50 bps hike to 1% and plans to reduce the balance sheet from 1 June. Despite the guidance to follow through with 50 bps hikes at the next two meetings, Fed Chair Jerome Powell said the Fed was not “actively considering” stepping up the pace of hikes by 75 bps. Investors cheered, and the Dow, S&P 500 and Nasdaq Composite rallied 2.8%, 3.0% and 3.2% respectively. Powell also affirmed that the committee estimated the neutral rate as 2% to 3% which should cap the 10Y bond yield at 3% and provide relief to Japanese officials fretting about excessive JPY weakness.

US markets are likely to be more data-dependent between now and the next FOMC meeting on 15 June. Tomorrow, US nonfarm payrolls might surprise on the downside. Yesterday, the ADP Employment Survey reported that 247k jobs were added in April, fewer than the 383k consensus and the 479k reported in March. The employment index in the ISM Services PMI fell to 49.5 in April, below the breakeven 50 level for the second time in three months. While employment in the manufacturing PMI remained positive, it did drop from 56.3 in March to 50.9 in April, its lowest level since September. Starting tomorrow, Fed officials will be lining up to speak with the narrative balancing between the Fed’s commitment to rein in inflation and its desire for a soft landing that Powell has described as looking “softish”. We see DXY consolidating between 102 and 104 for now and will consider a deeper correction if the focus shifts from the Fed to other central banks.

GBP appreciated 1.1% to 1.2631, above 1.26 for the first time since 25 April. The Bank of England meets today and is not expected to buck the tightening trend to fight inflation. Expect the committee to lift the bank rate a fourth time by 25 bps to 1%, its highest level in 13 years. Despite recession talk, CPI hit a 30-year high of 7% YoY in March amidst a two-year unemployment rate of 4.3% in March. Core inflation was also high at 5.7%, significantly above the 2% target. Two weeks ago, BOE Governor Andrew Bailey voiced concerns over persistent inflationary pressures, noting the labour market might stay tight for longer despite growth risks. Hence, GBP could correct up more to 1.27-1.28 if the BOE joins the Fed and other major central banks in becoming more duty-bound to rein in inflation. The market appears to agree and sees the BOE bringing rates above 2% a year from today.

Quote of the day

“Whenever you find yourself on the side of the majority, it is time to pause and reflect. ”

Mark Twain

5 May in history

Willie Mays hit his 512th home run in 1966.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.