Investing in Singapore Government Securities other than SSBs

![]()

If you’ve only got a minute:

- While the strong returns of SSBs have made headlines recently, the yields of SGS Bonds and T-bills have also been rising.

- T-bills are particularly useful if you are looking for very short-term investments from 6 months to a year without having to take on much investment risk.

- Set up a holistic plan that includes budgeting, protection and building a diversified portfolio that includes an optimal asset allocation into equities (for growth and to beat inflation) and fixed income securities like bonds and T-bills, and endowment plans to achieve financial wellness

![]()

Today’s volatile investing environment has led investors to adopt a “flight to safety” approach, manifested in a shift towards bonds and other safe alternatives. With inflation hitting all-time highs, more risk averse investors are realising that that they need to make their money work harder and are on the lookout for low-risk investment vehicles to park their savings.

As such, the Singapore Savings Bonds (SSBs) have seen increased uptake recently, but do you know that there are other Singapore Government Securities (SGS) that you can invest in? Below are 2 other types of SGS you can consider.

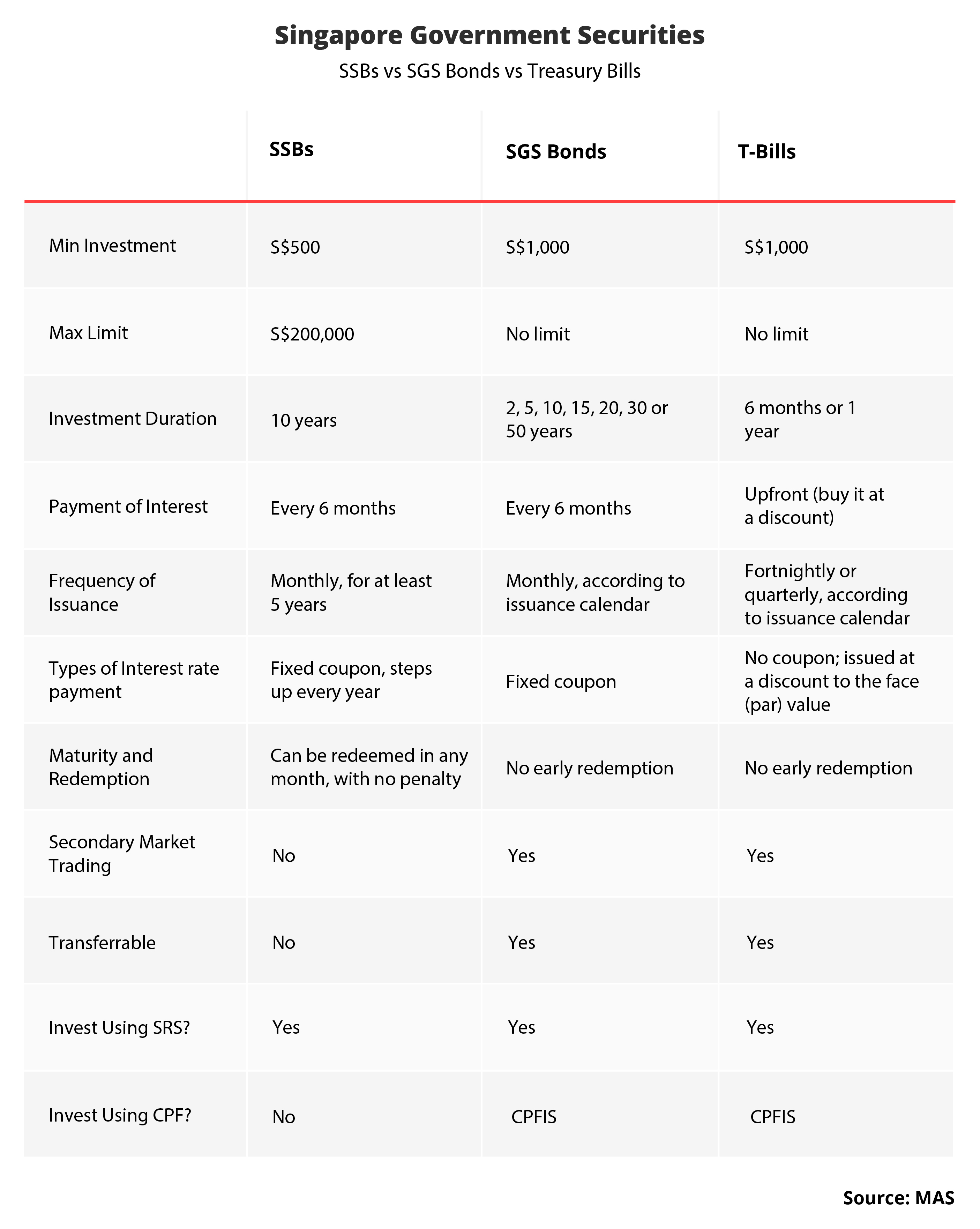

SGS are essentially government bonds issued by the Monetary Authority of Singapore (MAS) and are debt instruments with a AAA credit rating. What this means for investors is that securities issued by the Singapore government are among the safest investment offerings as they have a high degree of creditworthiness and a very low risk of default.

When you purchase a T-bill or bond, you are essentially lending money to the Singapore government over a predetermined timeframe. These borrowed funds can then be used for specific infrastructure projects or to develop the debt markets. Since each instrument boasts different features, the product that’s right for you will depend largely on your investment amount, time horizon and needs.

SSBs

To recap, SSBs are government bonds that offer risk-free step-up interest that is payable half-yearly over 10 years. This makes SSBs popular among individuals especially retirees who place a premium on flexibility, liquidity and need for recurring income. Capped at a maximum holding of S$200,000, SSBs can complement your other savings and investments as a safe way to save for the long term.

The average 10-year rate of returns for SSBs have been on a steady increase with the October tranche offering an average 10-year interest of 2.75% per annum (p.a.) and a 2.6% interest in year 1 alone. The August 2022 tranche had provided a higher 10-year average return of 3% per year but a lower coupon rate of 2% in year 1.

SGS Bonds

While the SSBs’ strong returns have made headlines recently, the yields of SGS Bonds and T-bills have also been rising.

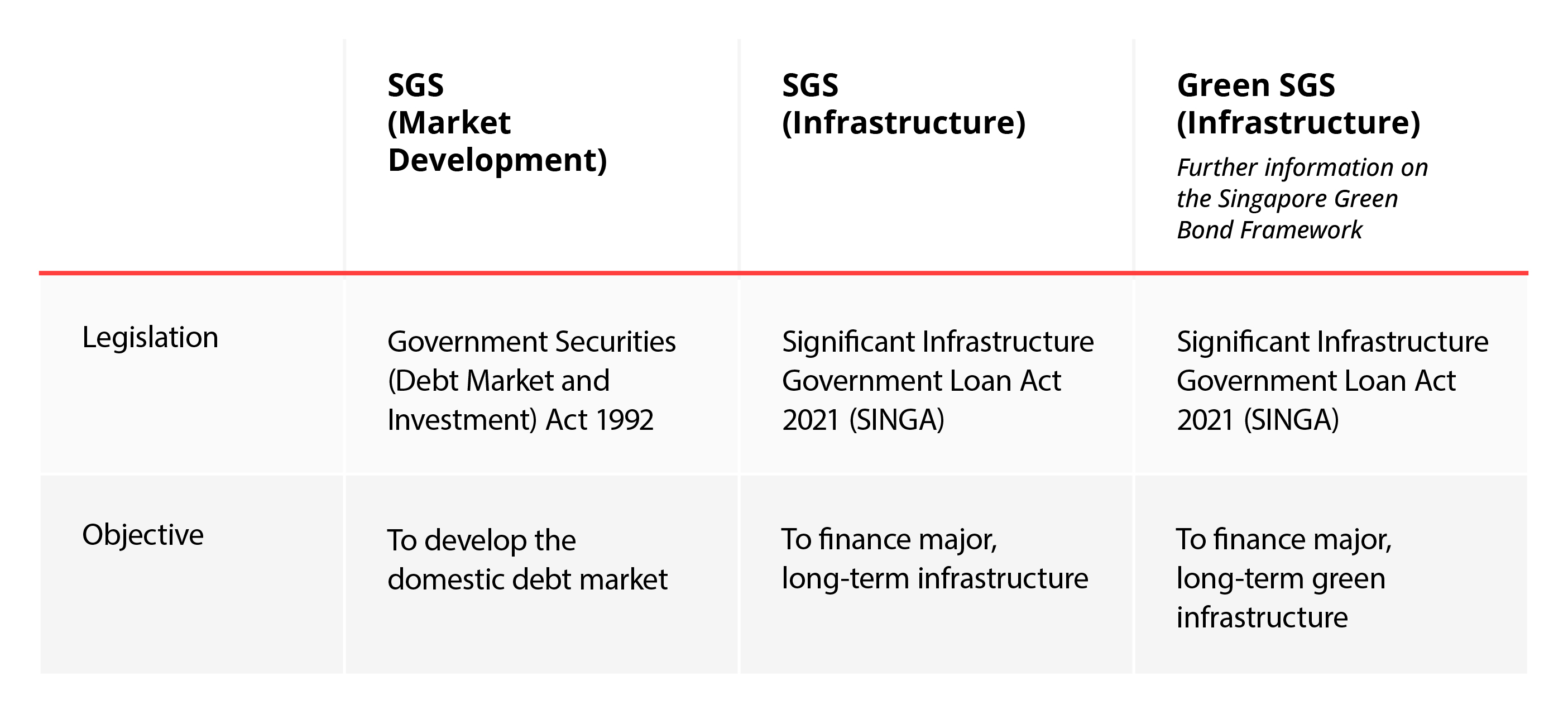

SGS Bonds are tradeable government debt securities that pay a fixed coupon every six months. They typically have a longer tenure ranging from 2 to 50 years and the three categories are: SGS (Market Development), SGS (Infrastructure) and Green SGS (Infrastructure) as shown in the table below.

Like SSBs, SGS bonds pay out regular interest payments (coupons) on the amount you invest in half yearly intervals throughout the bond tenor.

For example, if you had bought S$10,000 worth of the 50-year Green SGS bond with a coupon rate of 3% p.a., you would be getting S$300 in the form of two interest payments (S$150 each) every year. These payments will be made every half yearly until the bond matures (in this case 50 years – the longer you hold the bond, the more interest you will receive!).

If you decide to end the bond prematurely, you will have to sell it in the secondary market. Do bear in mind that the bond price may rise or fall before maturity.

T-Bills

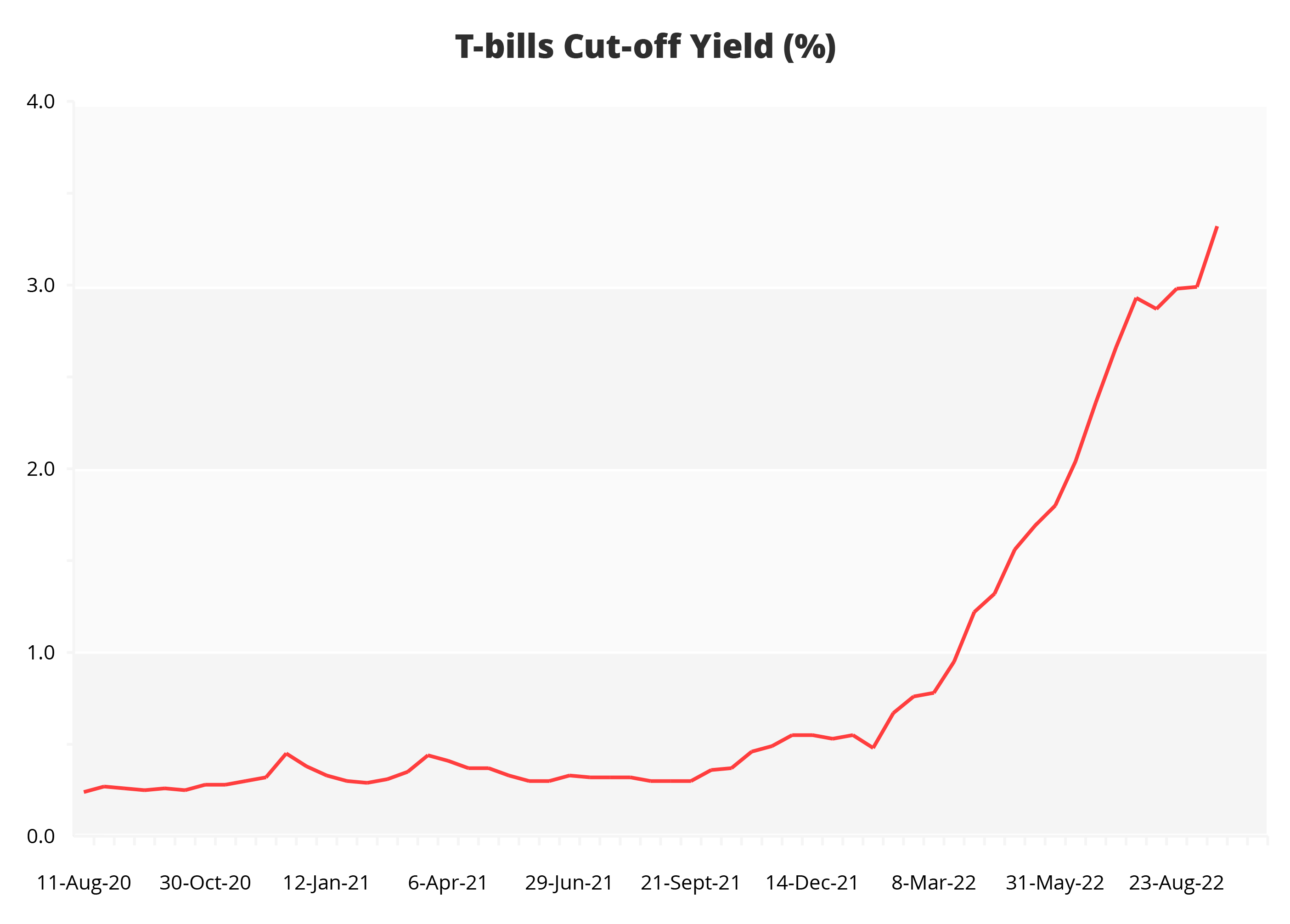

The 6-month T-bill issued on 15th September 2022 reached a high 3.32% cut-off yield, a significant increase from the previous T-bills issued on 6th September 2022 and 23rd August 2022, with cut off yields at 2.99% and 2.98% respectively. Unlike SSBs and SGS bonds, T-bills are zero-coupon bonds that do not pay out interest. Instead, they are issued at a discount.

For example, if you invest S$10,000 in a 1-year T-bill, you will receive the “interest” at the start (S$299 discount based on 2.99% p.a.) and eventually have your S$10,000 back at maturity. Put simply, you only need to pay S$9,701 upfront.

As T-bills are the shortest-term government securities available, they are particularly useful if you are looking for very short-term investments from 6 months to a year without having to take on much investment risk. They are a great way to park and grow your spare cash in the short term.

To sum up, here are 5 benefits of T-Bills and SGS bonds.

- Returns are better than plain vanilla savings accounts and higher than current fixed deposit rates

- Relatively short investment period

- The maximum amount you can apply under a non-competitive bid is S$1 million, starting with as little as S$1,000 (larger investible amount as compared to the S$200,000 cap for SSBs).

- Your principal is protected by the government

- T-bills are issued frequently enough for you to reinvest when they mature

The downsides of T-bills and SGS bonds include:

- No early redemption - you will have to sell them in the secondary market if you decide to terminate the bond early. Like other bonds, the SGS is subjected to market conditions and prevailing interest rates. If interest rates increase, the price of the bond may drop. Hence, if you do sell the bond prematurely, you might suffer capital loss.

- For T-bills, there is no guaranteed expected yield at the point of subscription since it is determined by the supply and demand at each auction. In other words, a sudden spike in the demand for the T-bill might result in a lower yield, which means you may not get your desired return upon successful allotment.

How can SGS fit into your financial plan?

SGS are relatively safe investment instruments with decent returns in the present high interest rate environment. Thus, you can put in spare cash that you do not need in the near future to earn higher interest rates.

Do however note that it may be challenging to sell your SGS bonds and bills on the secondary market, so you should carefully evaluate your liquidity concerns and take them into account.

Alternatively, you can consider investing your CPF monies in SGS bonds and T-bills so long as the returns exceed the OA’s risk-free return of 2.5% pa. Government securities are generally a safer alternative to protect the principal amount of your CPF monies. Do note that SSBs cannot be funded by CPF savings.

SSBs, SGS Bonds and T-bills are great options for those who desire to make their idle cash work harder by taking advantage of the decent yields coupled with negligible risk. These government securities also act as a springboard for you to start investing in riskier investments and are a great way to diversify your portfolio.

Though the rising returns of Singapore government securities and that of other low-risk instruments may look attractive, it is important not to put all your eggs into one basket. Speak with a DBS Wealth Planning Manager to review your financial goals and set up a holistic plan that includes budgeting, protection and building a diversified portfolio that includes an optimal asset allocation into equities (for growth and to beat inflation) and fixed income securities like bonds and T-bills, and endowment plans to achieve financial wellness.

![]()

This is the fourth article of our series on fixed-income investments. If you’re keen to learn more about this asset class as well as how you can invest in them, check out the other articles:

Part 1: A beginner’s guide to bonds

Part 2: 8 things to know before buying bonds

Part 3: Investing in SSBs

Part 5: Investing in T-bills

![]()

Ready to start?

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Need help selecting an investment? Try ‘Make Your Money Work Harder’ on DBS NAV Planner to receive specific investment picks based on your objectives, risk profile and preferences.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)