What can I do with my foreign currency?

![]()

If you’ve only got a minute:

- Foreign Currency Fixed Deposits (FCFDs) are a convenient option to getting returns on your foreign currency holdings.

- The interest on an FCFD is determined by the current interest rate environment.

- FCFDs come with an element of foreign exchange risk and are not covered by SDIC.

![]()

As a rather well-travelled bunch, it shouldn’t come as a surprise that many Singaporeans hold on to foreign currency either physically or in the bank.

In fact, most of us are familiar with heading down to the money changer to exchange currencies in preparation for work and/or leisure travel.

Today, most foreign currency transactions can be performed with a multi-currency account (MCA) like DBS Multiplier or DBS My Account. These allow you to hold up to 12 different currencies within one account with no foreign currency conversion fees charged. You can even pay directly from your foreign currency pocket by linking it to your DBS Visa Debit Card.

Other reasons for holding foreign currency include temporary overseas work relocations, sending money overseas to family members and when you make investments denominated in foreign currency.

If you do not have immediate needs for these foreign currencies, should they remain idle in your bank account?

Read more: Knowing the different types of payment cards

Find out more about: DBS Visa Debit Card – Your multi-currency card

What to do with idle foreign currency

When considering what to do with idle foreign currency, the first thing that comes to mind might be to convert it back to Singapore dollars (SGD).

Is this really the best choice? Well, it depends on several factors.

The most common factor is to check if the foreign exchange (FX) rates are in your favour, compared to what you initially converted it at. Do also consider why you are holding the currency, the amount you have on hand, and whether you have a use for it in the near future.

Some investors choose to use their foreign currency to buy into foreign currency denoted investments. For example, use US dollar (USD) to buy Apple shares or USD-denominated unit trusts. Others who expect their foreign currency to appreciate may wait for an opportune time to convert it back at a profit.

If you have no immediate needs for your foreign currency, an FCFD is a convenient way to gain a return on your funds while you wait to use it.

As with all investments, there is always an inherent element of risk involved. Anyone holding a foreign currency must be mindful that its value can fluctuate. It is helpful then to understand what impacts the value of currencies.

How are foreign currencies valued?

Most currencies are managed. This means that if needed, the central bank of the country can actively step in to influence its value against other currencies in order to manage volatility and uncertainty of the currency.

The supply and demand of a currency can be impacted through issuing new currency, setting interest rates, and managing foreign currency reserves. This in turn affects the value of the currency.

Some managed currencies include the USD, Euro (EUR), British pound (GBP), Japanese yen (JPY), and SGD, among others.

How is SGD managed?

As Singapore’s economy is highly dependent on trade, the Monetary Authority of Singapore (MAS) manages the SGD exchange rate to ensure price stability.

The SGD is weighted against a basket of currencies of our major trade partners and competitors. This trade-weighted SGD is known as the nominal effective exchange rate (S$NEER) which floats within a pre-determined policy band.

The MAS reviews this band twice a year and adjusts it when necessary, by buying or selling as much as is needed to keep the S$NEER within the band. This in turn will affect the price of the SGD on the FX market.

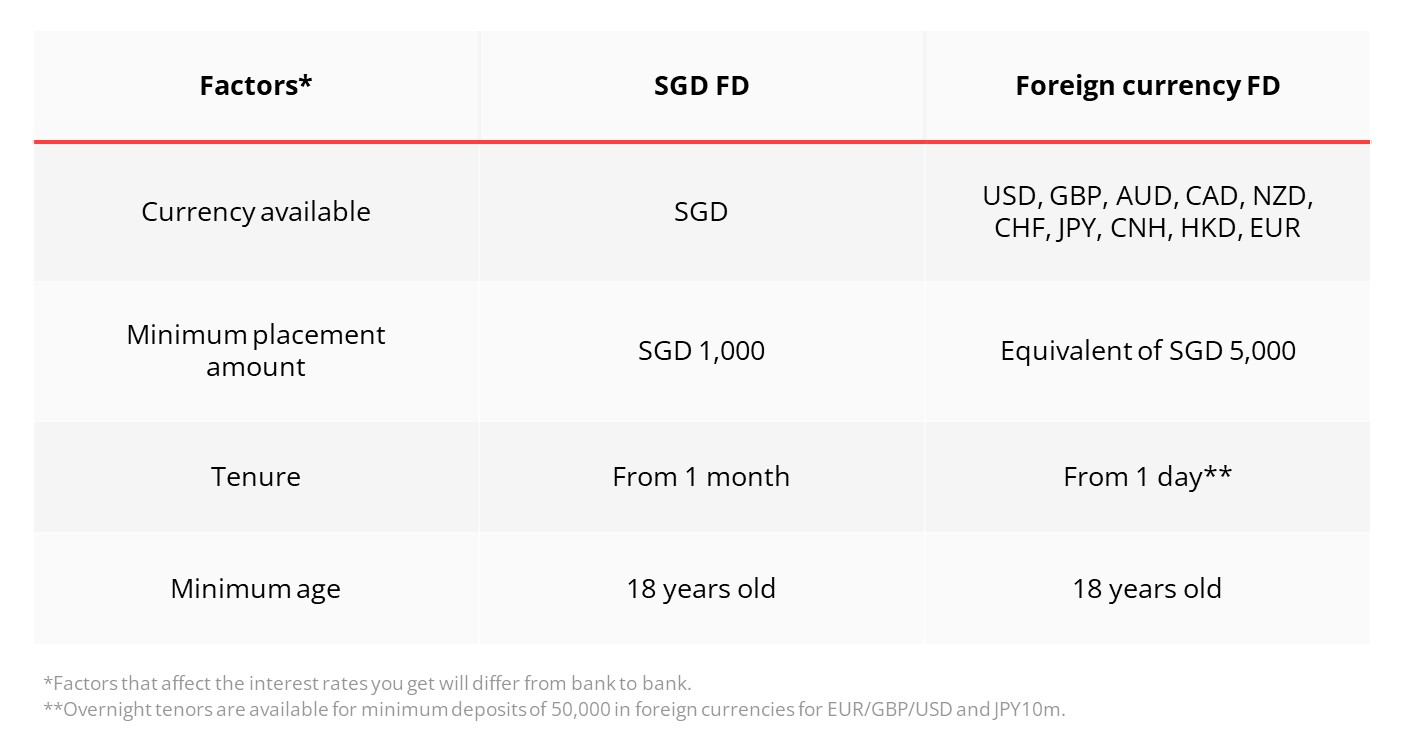

Foreign Currency Fixed Deposits

Similar to a SGD Fixed Deposit, with an FCFD, you lock your funds in a Fixed Deposit account for a set amount of time in exchange for a higher interest rate than the average savings account. Returns on an FCFD are dependent on the current interest rate environment when you make the deposit.

There are several ways to fund your FCFD. The most direct would be using any foreign currency you have on hand. Some investors choose to convert their SGD to foreign currency to take advantage of favourable exchange rates and interest rates.

This can also be done using funds from your Supplementary Retirement Scheme (SRS) if any. Note that upon maturity, the funds credited back into your SRS account will be in SGD. This means you will be subjected to the risk of exchange rate fluctuations.

It is good to check if your FCFD has an auto-roll feature. These provide convenience as you do not have to manually place the funds into a new fixed deposit upon maturity of the initial one.

However, they are done at the prevailing interest rates at the time of rolling over and you may be getting locked into a new fixed deposit at a less favourable rate if rates have fallen.

Find out more about: Opening a Fixed Deposit account

Benefits of FCFDs

Attractive interest rates

Foreign currency can be held in a multi-currency account like DBS Multiplier or DBS My Account but placing it in an FCFD will offer more attractive interest rates.

For example, at point of writing (7th December 2023), a placement of USD 10,000 for 2 months will offer an interest rate of 5.03% p.a., as compared to 0% on a USD savings account or 0.5% p.a. for an SGD placement with the same parameters.

Certainty of returns

As the parameters and interest rates are known and locked in at point of placement, there is no need for any active monitoring of your investment. You have certainty in knowing when your funds become available and the amount you expect to receive.

Easy roll-over

FCFDs allow you to roll-over your FCFDs into a new one if you are not ready to use your funds yet.

For example, if you find yourself holding currencies like the Australian dollar (AUD) and New Zealand dollar (NZD) which have fallen below parity to SGD in recent years, you can choose to place the funds in an FCFD. This way, you are not hard-pressed to convert the funds back to SGD at a loss.

Risks of FCFDs

Foreign exchange (FX) risk

Conversions between currencies involve fluctuations and are subject to exchange controls. If you are converting from another currency to place the deposit and intend to convert it to the original currency, exchange rate fluctuations could cause the converted amount to be less than your original amount.

Early withdrawal penalties

If you need to withdraw your funds before the maturity date, you risk losing the interest you would be earning on the deposit and may incur an early withdrawal fee. This may result in you receiving less than the principal amount in the currency of the deposit.

Not covered by SDIC

In the unlikely event of the bank defaulting, the Singapore Deposit Insurance Corporation (SDIC) does not cover foreign currency deposits. This means that if anything should happen to the bank you hold your deposits with, you can lose the full amount of your holdings.

Summary

FCFDs are a convenient way to put your idle foreign currency to work for higher returns until you need to use them. A DBS Fixed Deposit account can easily be opened with a few clicks via digibank mobile or online.

Remember to consider your time horizon and the corresponding stability of the currency before making a placement.

Check out the latest deposit interest rates on the foreign currency with DBS and consider locking in those attractive rates today!

Ready to start?

Need help selecting an investment? Try ‘Make Your Money Work Harder’ on digibank to receive specific investment picks based on your objectives, risk profile and preferences.

Invest with DBS Invest with POSB

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors and monies and deposits denominated in Singapore dollars under the Supplementary Retirement Scheme are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. Monies and deposits denominated in Singapore dollars under the CPF Investment Scheme and CPF Retirement Sum Scheme are aggregated and separately insured up to S$100,000 for each depositor per Scheme member. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)