Young parents: Protecting your finances with insurance

![]()

If you’ve only got a minute:

- Fortify your emergency fund with insurance plans such as endowment plans and other insurance plans, so you won’t need to dip into your hard-earned cash during times of need.

- Have adequate health coverage by having health insurance and personal accident plans, especially if you’re in a higher-risk job.

- An endowment plan is particularly useful when you have built your emergency fund and want to increase your savings.

![]()

This article was produced in partnership with MoneySmart.

Congratulations! So, you are now building/growing your emergency fund and you’re making steady progress.

As we mentioned in our emergency fund article, there is also a need to fortify/safeguard your emergency fund with insurance plans such as endowment plans.

We can take it one step further and add on other insurance plans to safeguard your hard-earned savings (because we know how costly medical bills can be and how difficult it is for one parent — if the other is sick — to take care of the household and juggle finances).

Why do I need to safeguard my savings?

When doing your financial planning, every budget carved out serves a specific purpose. For example, savings for your child’s future education, savings for your home renovation, savings for your retirement and of course, your emergency fund (liquid cash you may need for a rainy day, at least 3 months’ worth of your monthly expenses).

While you needn’t save for that S$5 economical rice you eat every day (though having a monthly food budget might be sound), it’s a good idea to save up for short- to medium-term planned purchases or expenses such as housing downpayments, education, a holiday, that Brompton bicycle, etc.

It doesn’t feel good if you need to channel some (or most) of your carefully planned and hard-earned savings for various goals into circumstances that you could have already been protected for, such as accidents or illnesses. That’s where the concept of safeguarding your money (and your goals) with insurance comes into play.

I got extra savings, is that enough?

Even if you have a million dollars stashed away in a biscuit tin under your bed, having savings alone is not enough. People tend to underestimate how much of a drain medical bills can be to your finances. I’m sure you would rather invest in property and let an insurance plan (comparatively much cheaper) take care of medical bills.

Having heavy financial obligations is also a stress point, especially when you’re the sole breadwinner of the family. By safeguarding your savings, you could enhance your ability to bounce back healthily and financially quicker (because you used insurance money and not your own savings).

Mind the gap

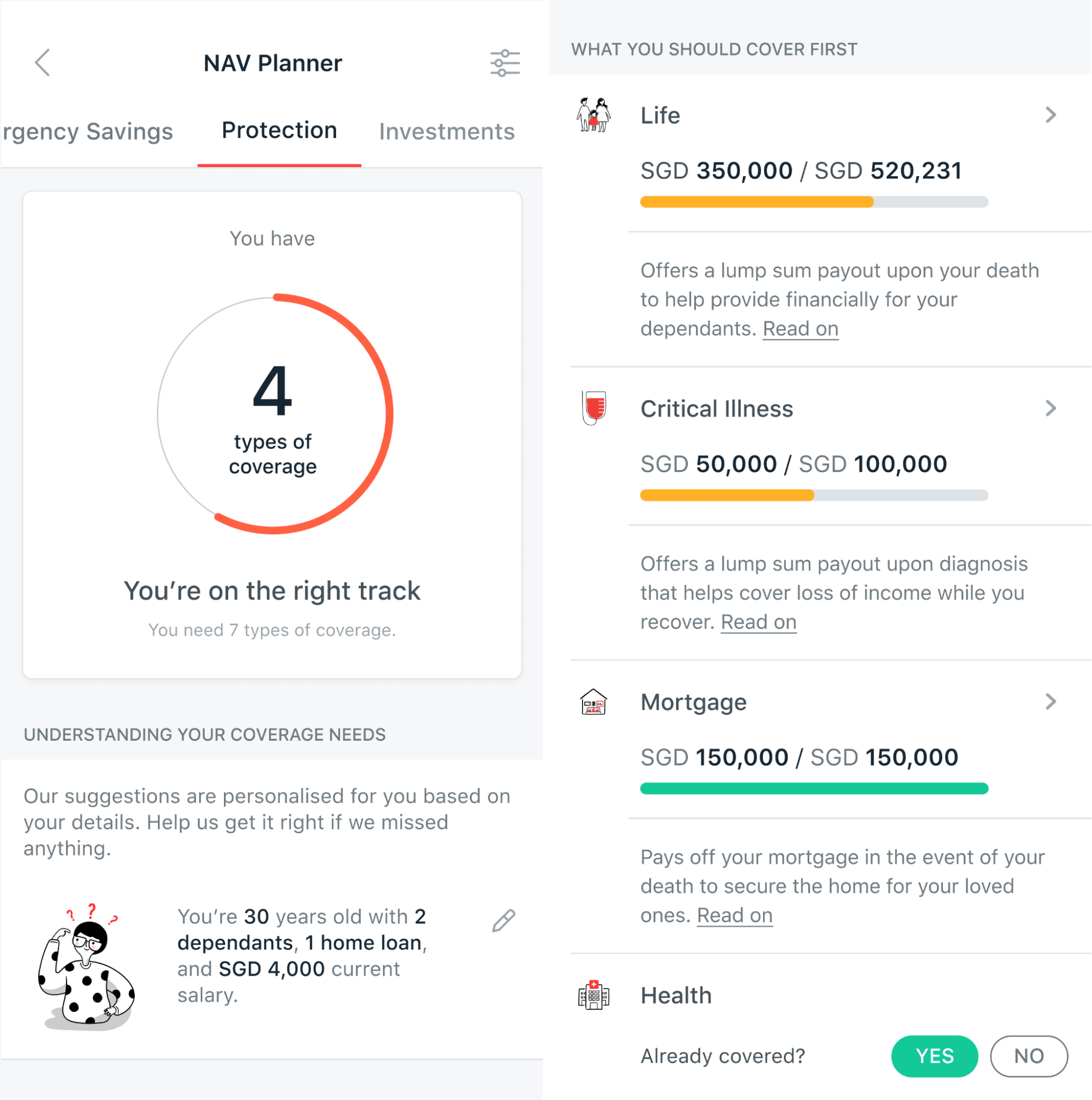

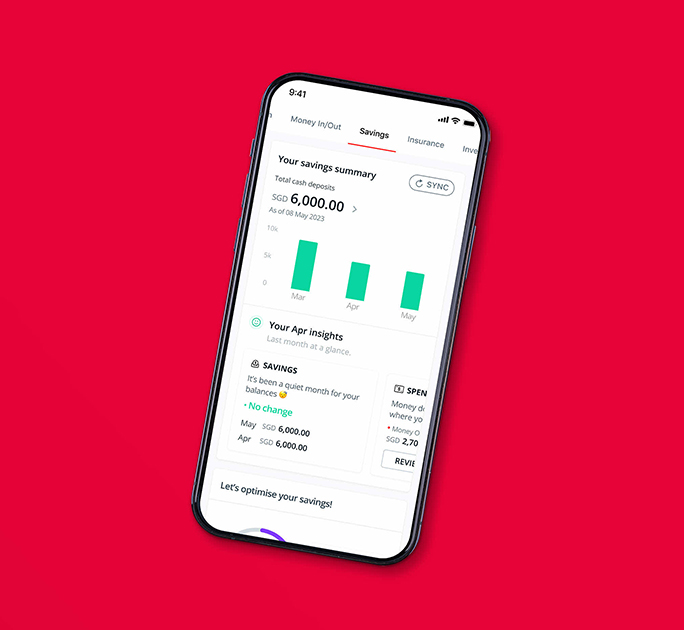

If you’re unsure if you have any protection gaps, a handy feature in the Plan & Invest tab in digibank tool is the Protection Room. Here, you can input info such as your dependents’ details and existing insurance plans, PLUS pull data from SGFinDex (if you’ll allow it to). With this, Plan & Invest tab in digibank can correctly size your existing assets and automatically calculate your gap based on your liquid assets, dependents’ info and existing protection plans (such as health insurance, personal accident, life, term, etc). Hurrah!

Here are some ways to safeguard your savings with insurance, so you won’t need to dip into your hard-earned cash during times of need.

Have adequate health coverage

Health insurance plans typically cover a wide range of things, including hospitalisation and surgery, critical illness, medical treatments, post-hospital treatments, out-patient procedures and treatments, rehabilitation, seeing a specialist, and more. This could also include worldwide cover, ambulance fees and a lump-sum payout.

It’s also good to have a personal accident plan too, especially if you’re in a higher-risk job (such as in a restaurant kitchen or in a factory). Some plans such as MultiGen Protect even allow you to get tailored coverage for the whole family, and cater specifically to the type of protection required by the adults, kids, and grandparents.

Health coverage also extends to long-term care, such as chronic diseases, long-drawn treatments or disability that affects one’s ability to be independent.

Meanwhile, the person who is injured or unwell will be unable to provide for his/her family, so that’s where lump-sum payments are useful.

All of these can cause a big financial drain, and unless you are a billionaire, all of your life’s savings alone aren’t enough to cover these costs.

By having adequate health coverage, you won’t need to draw from your own savings — hence safeguarding them.

Tip: You can use Plan & Invest tab in digibank’s “Make Your Money Work Harder” feature to learn more about different insurance products, including endowment, investment-linked policies, income stream products and more. These insurance products could help you further fortify your hard-earned savings.

Endowment as a complement to your savings

An endowment plan is one where you put money into (single or regular premium), wait for it to mature, and then take out the lump sum, which comprises both guaranteed and non-guaranteed returns. As this is an insurance plan, it typically comes with some protection, which can be helpful too.

Having an endowment plan is particularly useful when you have built your emergency fund and want to fortify it further.

Some reasons why people buy endowment plans include retirement, education (your further education or your child’s) or an income stream (the endowment plan doles out regular payouts after a certain point).

If the endowment policy allows, you can even tailor it to specific needs. For example, your child is now 8 years old and you want to prepare for his/her university education 20 years later. You can buy an endowment fund such as SavvySpring (II) to supplement that savings goal — when it matures 12 years later, the maturity payout period aligns with your child’s university education.

Similarly, if you’re getting an endowment plan for retirement, SavvySpring’s customisable premium payment term could come in useful. You can choose to pay premiums for just 3 or 6 years, leaving the Guaranteed Cash Benefit1 to take care of premiums until the policy matures.

Tip: Determine the annual premium amount (minimum S$2,381) by considering what age you’d like to retire at, how much you need for retirement (taking into consideration your CPF monies and other assets) and build this into your endowment plan. Not sure how to visualise this? Plan & Invest tab in digibank (available through your digibank) can show some estimates of how much you might need and/or the shortfall (if any).

Protection is an ongoing process

At this point, even if you’ve addressed all of your protection gaps, you’re not done. One’s protection needs might change at different life stages — and if you have a family, you’ll know that your growing children’s needs will change too.

Just like we go for health check-ups, make it a point to re-assess your needs and re-examine your coverage every few years. You can do this via your Plan & Invest tab in digibank tool or seek the advice of a financial advisor.

For example, you might use Plan & Invest tab in digibank’s Protection Room to make your existing plans more robust (such as term life, personal accident, mortgage insurance), or beef up protection with home contents insurance (insures the contents of your home as well as protects the inhabitants), get a Careshield Life supplement, increase your sum assured (especially if you signed up for a life insurance plan in your early 20s and now you’re at the lifestage where you need more coverage as you’re preparing to start a family, buy a house and so on), etc.

With Plan & Invest tab in digibank’s Make Your Money Work Harder feature, you can learn more about insurance plans that can help income growth, such as endowment products like SavvySpring (II) that we’ve mentioned earlier.

Go on, safeguard/fortify your savings with an insurance plan such as SavvySpring. It’s time to ride the Ox by the horns this year — make sure your protection is solid, without any gaps or weak points in your armour.

Ready to start?

Check out digibank to analyse your real-time insurance coverage. The best part is, it's fuss-free - we automatically work out your gaps and provide planning tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)