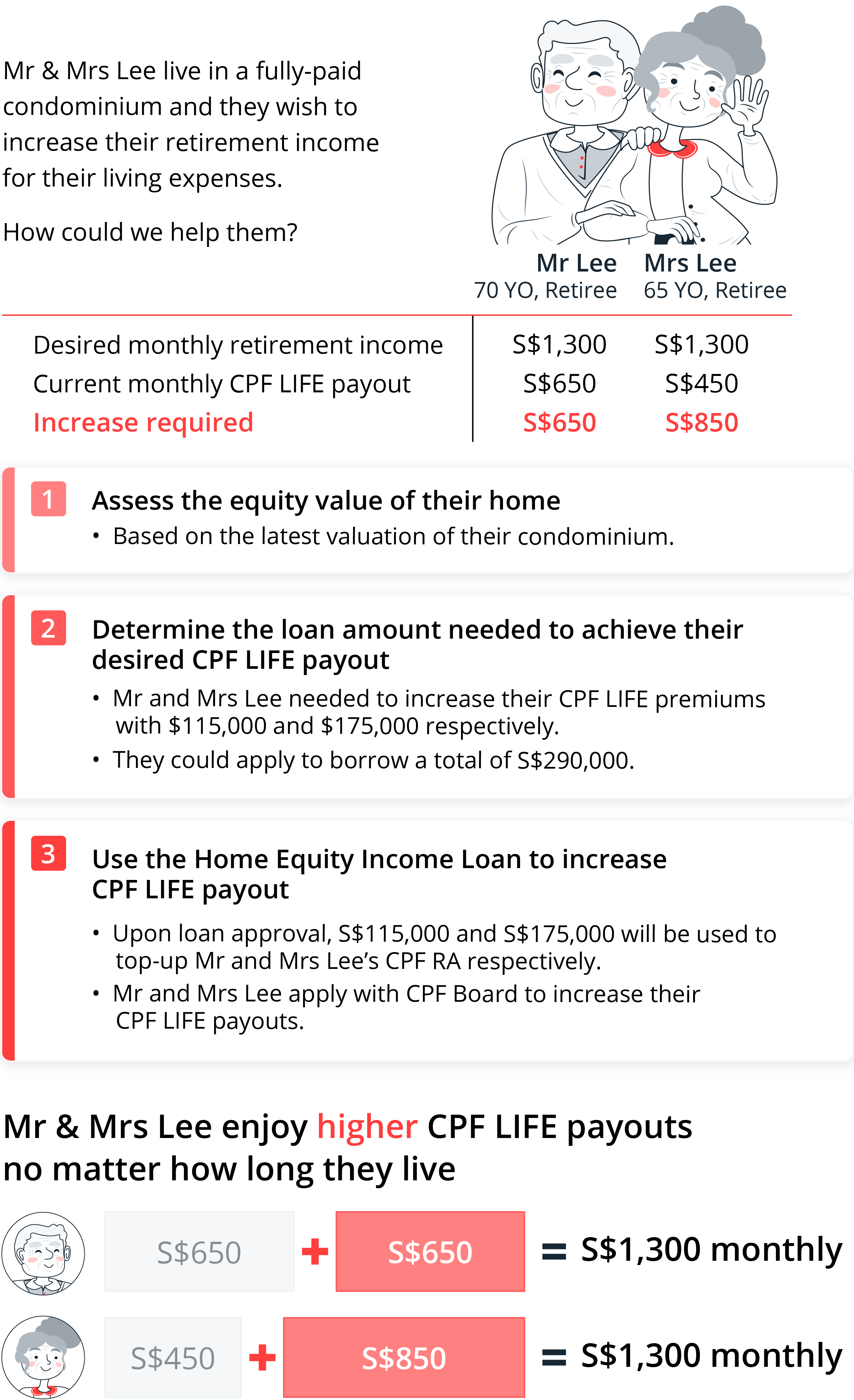

Unlock value from your home with a loan

Lasting Power of Attorney (LPA)

- Must set up a Lasting Power of Attorney (LPA). Find out more about why LPA is important here.

- If you have not set up an LPA, we could assist you as part of this loan application.

Property and Tenure

- If it is a leasehold property, the remaining lease of the property at the end of the loan period must be at least 30 years.

- Any outstanding CPF charges on the property must be discharged (we will assist you as part of this loan application). This ensures that you could obtain the loan amount to increase your CPF LIFE premium sufficiently.

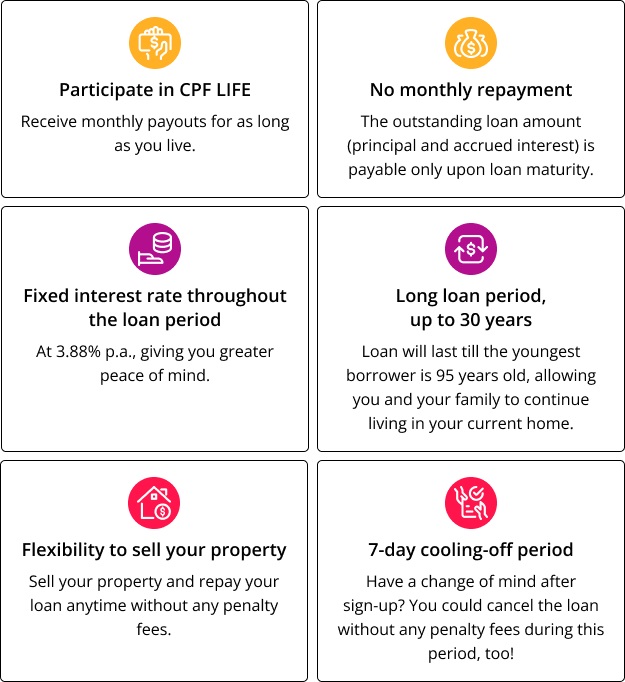

CPF LIFE and Retirement Account (RA)

- The loan amount will be used to directly top up your CPF Retirement Account for payment towards CPF LIFE premium.

- The monthly payouts from CPF LIFE must be credited to a DBS/POSB account.