- Industrial economy growth would slow sharply due to high interest rates even as inflation ebbs

- China’s growth will recover, but many internal and external headwinds persist

- For Asia ex-China, growth will be weighed down by weak exports, but reopening momentum to remain

- We don’t expect a prolonged downturn; global growth to rebound in 2024 with lower rates and inflatio

- Risk is we are too pessimistic about 2023 and too optimistic about 2024

Commentary: Outlook for 2023-24

The procession of global outlook reports from multilateral agencies underscores deep concern about the outlook. The widespread view is that macroeconomic risks remain unusually large, ranging from getting US monetary policy stance wrong to tightening global financing conditions triggering emerging market debt distress, not to mention a worsening of China’s growth dynamic around a weak property sector and continued struggles with the pandemic.

We recognise these risks and have incorporated them in our forecasts for 2023 and 2024. For next year, we see growth slowing sharply in the US (from 1.5% this year to roughly flat in 2023) and EU (from 3.2% this year to a small contraction next year). The US would be facing the lingering effects of substantial policy tightening, with real rates rising by more than 200bps through the course of 2023, as nominal policy rate holds at 5% while inflation eases gradually. As for EU, the energy price and sentiment shock emanating from the war in Ukraine is bound to drag down growth. Typically, China is a critical balancing factor during global cyclical weakening, but this time it has its hand full, with a myriad of internal and external headwinds. We see no more than 4% growth there in 2023.

In Asia ex-China, the prospects are mixed. Growth will be subtracted by weak exports, which is already the making. But the region is in the middle of a strong re-opening dynamic, with travel, tourism, and events surging, all proving to be resilient despite the sharp increase in cost of living. We attribute this to relatively healthy household balance sheets in the region. Taken together, we expect Asean-6 growth to ease of 4.8% next year, from a projected 5.8% this year.

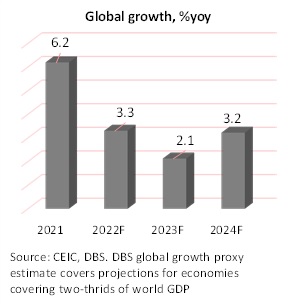

All in all, we are projecting a sharp decline in global growth next year, but we don’t expect lasting economic slowdown. After slowing to 2.1% next year, global demand would turn around in 2024, growing by over 3%. This would take place as US monetary policy is eased, lowering the cost of funding worldwide, China’s macro and public health fundamentals undergo a rebound, and energy markets see considerable easing of supply chain pressures.

What are the chances of this narrative being wrong? Quite a bit, we’re afraid. Firstly, 2023 may turn out to be better than feared, as consumers, by virtue of their balance sheets being in sounder health than they were during the 2008 Global Financial Crisis, may end up demonstrating a surprising degree of demand resiliency despite higher rates. Meanwhile, 2024’s recovery narrative may be undermined by the lagged effect of ongoing rate hikes, which the Fed won’t be able to offset as its room to cut rates may be limited by still-2%+ inflation. War, pandemic, and great power rivalry may be additional spoilers.

Taimur Baig

To read the full report, click here to Download the PDF.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.