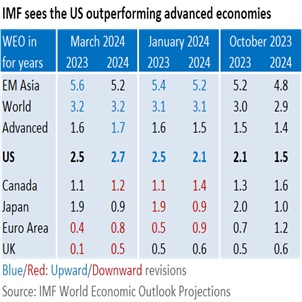

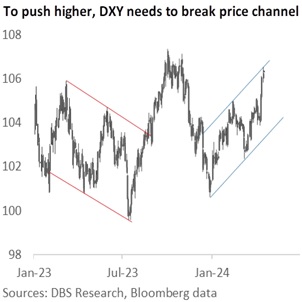

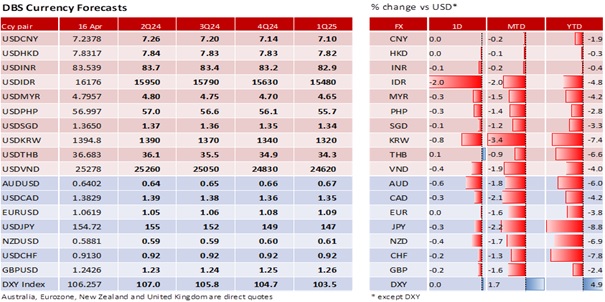

DXY appreciated 0.14% to 106.36, holding above 106 for the third session. The IMF World Economic Report now forecasts US GDP growth accelerating to 2.7% in 2024 from 2.5% in 2023, in stark contrast to last October’s projected slowdown to 1.5% from 2.1%. More importantly, the new US growth forecast is significantly superior to those projected for the Euro Area, Japan, the United Kingdom, and Canada. By contributing most to the upgrade in world GDP growth this year, the US economy is maintaining its exceptional performance and keeping the USD strong against the JPY, EUR, GBP, CAD, and Emerging Asian currencies this year. Against this background, the currencies at risk are those looking to cut rates before the Fed.

The US Treasury 2Y and 10Y yields firmed by 7 bps each to 4.99% and 4.67% in the overnight session. Fed Chair Jerome Powell acknowledged that the Fed lacked the confidence to lower rates anytime soon based on the recent strength in US labour market and inflation data. Powell signalled that the Fed could keep interest rates restrictive at the current level for “as long as needed” to return inflation to the 2% target. The Fed will enter a blackout period next week before the FOMC meeting on May 1. Interest rate futures see a 43% chance of a delayed first cut in September and 48% odds for a second reduction in December. Following Powell’s comment, the odds have increased for the Fed to dial down the three rate cuts for 2024 in the June Summary of Economic Projections. In June, expect more than nine of the 19 Fed officials who wanted two or fewer cuts in March.

In the short term, currencies stabilized somewhat after the panic selling on Monday and Tuesday due to fears of a broader conflict in the Middle East. US stock market futures are looking for a positive open today after the Dow Jones Industrial Average closed higher for the first time in seven sessions. Investors will pay close attention to oil prices and how Israel will retaliate against the unprecedented drone and missile attack from Iranian soil. The IMF estimated that a sustained increase in oil prices by about 15% would lift global inflation by about 0.7%. The Israeli war cabinet has put off a third meeting until today amid efforts by the US and allies to avert a major escalation. US Treasury Secretary Janet Yellen indicated further sanctions against Iran in the coming days. The Israeli Foreign Ministry pledged to lead a diplomatic attack by writing to 32 countries, asking them to place sanctions on Iran’s missile programme. The geopolitical situation remains fluid, keeping markets on the edge.

Quote of the day

"Given the strength of the labour market and progress on inflation so far, it is appropriate to allow restrictive policy further time to work and let the data and evolving outlook guide us.”

Fed Chair Jerome Powell, 16 April 2024

17 April in history

The funeral of Prince Philip, Duke of Edinburgh, took place at St George's Chapel, Windsor Castle in 2021.

Topic

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). This report is intended for “Accredited Investors” and “Institutional Investors” (defined under the Financial Advisers Act and Securities and Futures Act of Singapore, and their subsidiary legislation), as well as “Professional Investors” (defined under the Securities and Futures Ordinance of Hong Kong) only. It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 13th Floor One Island East, 18 Westlands Road, Quarry Bay, Hong Kong SAR

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.