Fuelling Asia’s decarbonisation with green ammonia and hydrogen

Fuelling Asia’s decarbonisation with green ammonia and hydrogen

Just as the cost of solar and wind energy eventually surpassed grid-parity after early reliance on feed-in tariffs, green ammonia is now following a similar trajectory.

Please use valid input

Please fill in for one-time registration. Thank you!

By Xueyong Chin, Senior Vice President, Project Finance, and Lakshmi Natarajan, Vice President, Project Finance, DBS Bank.

This article is also published in PFI Yearbook 2026.

The global energy transition is accelerating, driven by climate change and energy security concerns. Green hydrogen and its derivative, green ammonia, are emerging as critical and promising solutions for decarbonising hard-to-abate sectors such as heavy industry, maritime shipping, and power generation. This transition holds particular promise for Asia, a region poised to lead in scaling green ammonia adoption and advancing policy frameworks.

Asia’s surging energy demand, robust industrialisation, and strong decarbonisation commitments are catalysts for ambitious national strategies and cross-border collaboration.

Green hydrogen offers a route to decarbonise industrial processes such as steel and chemical production, replacing fossil fuel inputs. Green ammonia is also gaining traction as a maritime fuel, critical for decarbonising global shipping. Both also serve in power generation, co-firing with fossil fuels or fuelling dedicated or mixed-fuel turbines to provide dispatchable, carbon-free electricity, complementing intermittent renewables.

Ammonia’s stability also makes it excellent for long-duration energy storage. Considering the various applications, the global green hydrogen market is expected to grow from about 0.5m tonnes per annum (Mtpa) in 2025 to around 6.1Mtpa in 2030.1 While it is several times more expensive today, green ammonia could become even cheaper than natural gas-produced grey ammonia in some markets by the mid-2030s.

Major Asian economies are actively recalibrating their energy strategies

As the cost gap between ammonia and other energy sources narrows, major Asian economies are actively recalibrating their energy strategies.

Japan aims for net-zero by 2050, centralising hydrogen and ammonia for power and heavy industries. Large-scale ammonia co-firing in power plants is a primary goal, with projected ammonia demand for generation potentially reaching 30 Mtpa by 20502.

South Korea’s comprehensive Hydrogen Economy Roadmap projects a significant uptake of hydrogen for power generation, alongside ambitious overall demand targets of 3.9Mtpa by 2030 and 27.9Mtpa by 20503, driven by power generation, industrial decarbonisation, and mobility.

Singapore is positioning itself as a regional green energy hub, exploring green ammonia for maritime bunkering, power, and industrial feedstock. Neighbouring countries such as Malaysia, Indonesia and Vietnam are exploring domestic production and imports for power decarbonisation, driven by rapid industrialisation.

Limited domestic renewable resources, high energy import dependency and land scarcity in these industrialised nations necessitate significant imports.

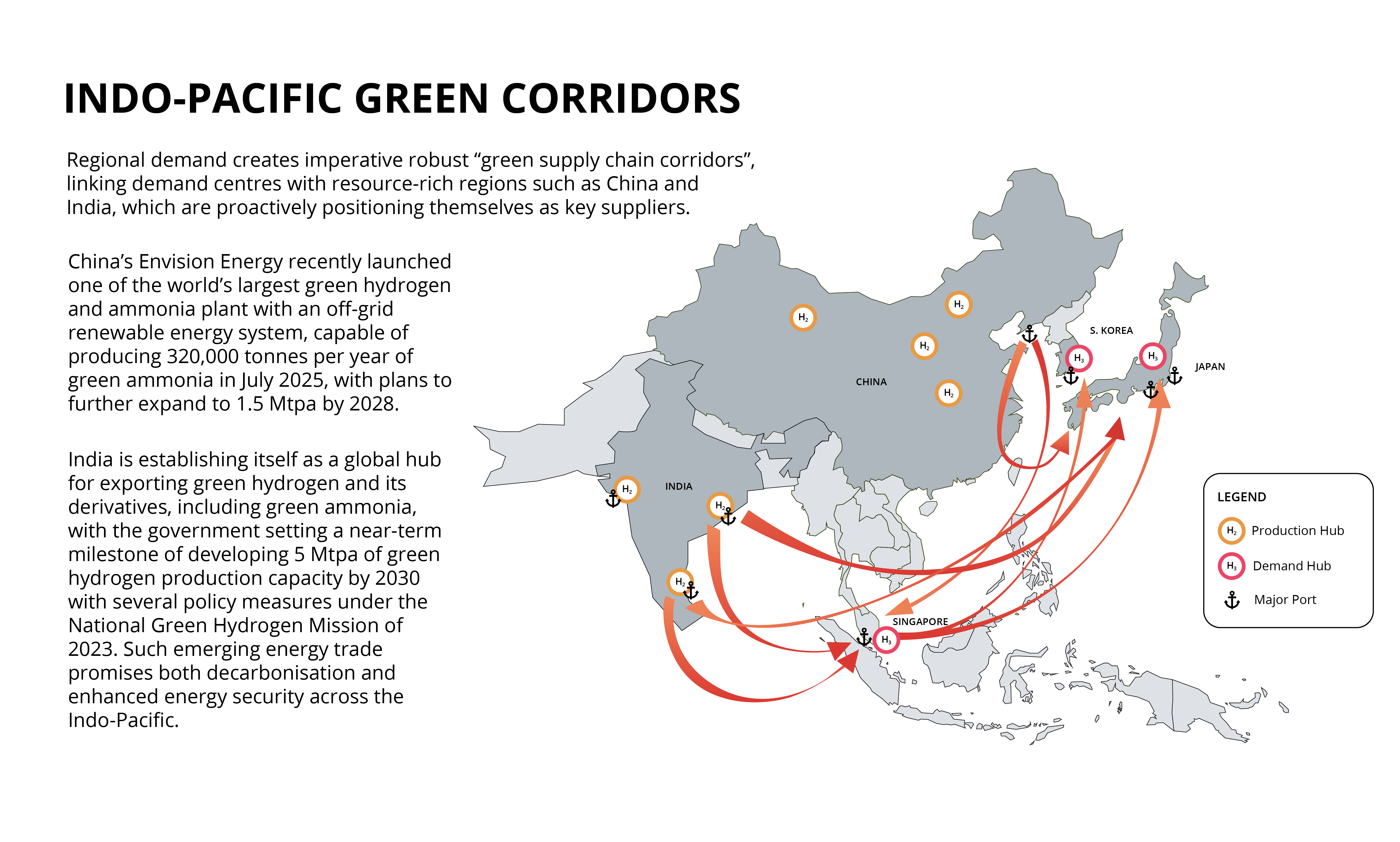

Navigating the supply chain imperative: Catalysing green corridors

The convergence of falling production costs, driven by abundant low-cost renewables, and proactive government support are accelerating the green hydrogen and ammonia toward cost parity with fossil-based alternatives.

Much like the early days of solar and wind, where feed-in tariffs helped catalyse scale and investor interest, green hydrogen and ammonia are now benefiting from similar policy mechanisms that are derisking early investments and unlocking market momentum on both the supply and demand side.

As the sector matures, the challenge will shift from proving viability to scaling sustainably. This calls for coordinated action across governments, industry, and financiers to build robust infrastructure, harmonise standards, and structure bankable projects.

Capital cost competitiveness

A pivotal consideration is achieving cost competitiveness for green molecules. Initial capital expenditure for gigawatt-scale plants remains substantial. To ensure that green ammonia can be produced round the clock via green energy, energy storage systems and grid integration are crucial.

Developers also need to ensure that the renewable energy capacity used to drive the green hydrogen/ammonia production is significantly oversized. For example, setting up a 100kt per annum ammonia plant typically requires about 500MW to 1GW of renewables, depending on the specific solar-wind-storage mix. This often results in higher costs compared to stand-alone renewable energy projects, which is challenging in Japan given high population density and limited land for the development of land-based renewables.

Similarly, market dynamics and grid infrastructure make renewable energy projects very expensive, creating an imperative for relying on imports from areas such as India and the Middle East. For new project development in India, land acquisition and grid availability are becoming increasingly challenging.

Expansion of transmission and substation infrastructure has not kept pace with the growth of renewable energy and developers find it increasingly challenging to secure evacuation approvals, resulting in significant delays and cost increases. Given that renewable energy generation is the underlying foundation for generation of green ammonia/hydrogen, these project-on-project risks impact the bankability of projects.

Regulatory and policy harmonisation

To create an efficient market, the immediate priority is developing globally accepted certification and verification standards for green hydrogen and ammonia. While different countries have introduced green hydrogen/ammonia standards, it would be critical to ensure that there is some harmonisation at a global level to allow marketability of the produced green hydrogen/ammonia across multiple jurisdictions, particularly given the relatively short-tenure offtake contracts of 10-15 years that are currently available.

For instance, South Korea’s Clean Hydrogen Portfolio Standard (CHPS) employs a well-to-gate approach with specific carbon intensity grades for eligibility in power generation while EU has its own Renewable Fuels of Non-Biological Origin (RFNBO) definition. Indian standards, on the other hand, are focused on domestic green hydrogen production and are still developing the certification frameworks for export.

On the supply side, some Indian developers are proactively developing projects compliant with international standards to gain access to international projects. For instance, AM Green is developing its Kakinada project to be compliant with EU standards for RFNBO, while Envision Energy’s green ammonia plant has been awarded the Renewable Ammonia Certification from Bureau Veritas, and recently obtained the ISCC Plus certification and confirms that the design would produce RFNBO. Such certifications ultimately serve to enhance the bankability of the projects by providing international credibility and transparency around the quality, safety and sustainability standards of the product, ultimately ensuring that the molecules can be sold to and used by even the most stringent of end-users.

Infrastructure and logistics

Establishing green corridors requires developing new supply chains, from gigawatt-scale renewable farms and electrolysers in supply regions such as India, to specialised transportation infrastructure. This necessitates significant investment in port upgrades for cryogenic storage, handling equipment, and dedicated berths in both producing and consuming regions, enabling efficient loading/unloading of large-scale ammonia carriers. While the development of dedicated upstream/downstream facilities could introduce additional operational and cost complexities, a strategic approach to achieve export scale lies in developing common infrastructure. Establishing intra-port pipelines, shared storage tanks, desalination systems and bunkering facilities could play a major role in enabling cost competitiveness in the long term.

The Indian government has also recognised the export opportunity and is looking at developing the necessary infrastructure. In October 2025, the Ministry of New and Renewable Energy formally designated three major ports in Gujarat, Tamil Nadu and Odisha as Green Hydrogen Hubs under the country’s National Green Hydrogen Mission (NGHM). Launched in January 2023 with an initial outlay of Rs197.44 billion (US$2.4 billion), the NGHM is a significant initiative supporting its green molecule ambitions. This policy targets the transformation of India into a global hub for green hydrogen production, utilisation, and export. It targets at least 5Mtpa of green hydrogen production by 2030 with potential for 10 Mtpa, supported by 125GW of associated renewable energy capacity.

It projects over US$100 billion in investments and over 600,000 jobs. Crucially, the NGHM includes strategic interventions such as the SIGHT programme, offering financial incentives for electrolyser manufacturing and green hydrogen production to significantly drive down costs and foster a robust domestic industry.

On the import side, Japan and South Korea are upgrading ports for green ammonia imports by developing new storage tanks, unloading facilities, and co-firing infrastructure, particularly in ports such as Yokohama, Kobe, Onahama, and Ulsan.

Similarly, Singapore is advancing initiatives as part of its national hydrogen strategy, which includes studies on developing a low or zero-carbon ammonia solution on Jurong Island for power generation and bunkering.

The Chinese government established its medium and long-term plan for the development of hydrogen energy, which aims to produce 100,000 to 200,000 tonnes of low-carbon hydrogen annually by 2025 and to create a diverse hydrogen ecosystem across transportation, energy storage and industry sectors by 2035. On top of providing subsidies to support technological innovation and encouraging regions top support hydrogen production powered by renewable energy, it also places emphasis on promoting standards and certification to enable greater utilisation by end users and acceptance on the export markets.

China is currently on track to achieve its initial targets at end of 2025, and the National Energy Administration had recently announced the first eight green methanol and green ammonia pilot projects that will be given priority to receive state support, subject to achieving high and stable production by June 2027.

Other than the recently commissioned phase 1 of Envision Energy’s Chifeng facility, the China Energy Investment Corporation was also given approval in August 2025 to begin construction on a 2.2GW green hydrogen-to-ammonia in Inner Mongolia. Similar to India, China enjoys large penetration of renewable energy, especially in regions like Inner Mongolia due to very high and underutilised wind and solar capacity, leading to competitive green ammonia prices, with long term offers below US$600 to US$700 per tonne FOB.4

Financing

These intertwined enablers, that is, achieving cost competitiveness and developing infrastructure to regulatory and technological maturation, along with social/environmental considerations – collectively amplify financing challenges, particularly for large-scale, first-of-a-kind projects seeking limited recourse financing. The integrated nature of green hydrogen/ammonia projects, encompassing renewable power, electrolysis, ammonia synthesis, storage and logistics requires a tailored approach from traditional project finance.

Unlike renewable energy, the offtake arrangements for green hydrogen/ammonia projects tend to be much shorter given the expectation of continued future cost reduction. This reduces their bankability as lenders would typically not be willing to take merchant risks in an emerging sector.

Uncertainty around long-term pricing, off-take bankability, technology risks, and regulatory uncertainty require lenders to seek strong government support, creditworthy off-takers, or extensive derisking mechanisms for non-recourse/limited-recourse debt. This is especially true given the lack of extensive historical operational data.

As with any large-scale deployment of new technologies, strong government support on both the policy and cost affordability fronts are typically required to make commercial and revenue models work in order to attract private capital from investors and their lenders.

Implementing mandatory consumption obligations for green hydrogen and its derivatives, supported by long-term off-take contracts with industries such as fertilisers and refineries – similar to renewable purchase obligations – could effectively stimulate demand. Governments in Japan and South Korea, for example, are stepping up with contract for difference (CfD) subsidy schemes to bridge the price gap.

Such government-backed, long-term CfD schemes provide much needed support for the price gap between sourcing low-carbon hydrogen/ammonia derivatives and traditional fuels (for example, natural gas) which helps to derisk investment by providing lenders and developers certainty around price and volume, which ultimately enhances the bankability of projects looking to supply under such schemes.

While South Korea’s recent announcement to cancel the second round of the CHPS tender does create some policy uncertainty, the market remains hopeful of the long-term potential of the sector, with new announcements of projects from China’s CEEC Songyuan Park, MHI and Nippon Shokubai’s partnership to develop an ammonia cracking system, and Sembcorp’s signing of a memorandum of understanding with the Paradip Port Authority in India to develop an integrated green hydrogen and ammonia ecosystem at the port in Odisha, India.

Putting it all together, there exists sufficient catalysts for developing and financing export oriented projects within the Indo-Pacific green corridors – for example green ammonia projects in India exporting to Japan or South Korea under the CfD schemes – where the combination of local policies enabling investment and lowering capex, and offtake enabling mechanisms to provide certainty of long-term cashflow allows projects to be commercially viable.

Apart from bridging the affordability gap for the green molecules, bridging the capital gap required to develop the upstream and downstream infrastructure for such first-of-its-kind projects will require tapping into various sources of funding across the entire capital stack.

Leveraging blended finance structures combining public, private, and philanthropic capital, along with active engagement of multilateral development banks and international financial institutions, is critical to derisk projects, mobilise private investment, and secure necessary capital at acceptable terms for these multibillion-dollar endeavours.

For example, India’s introduction of capital subsidies and budgetary allocation to develop supporting infrastructure does provide a positive signal to the market. Though projects remain in early stages, there is a significant interest from all stakeholders to develop bankable financing structures. Developers are also looking to tap into export credit agency-backed financing to help optimise financing costs.

In addition to traditional export-based financing support, several ECAs, notably those of South Korea and Japan, have also established frameworks to support the import of strategic resources into their respective countries, further derisking projects for lenders and ultimately serving to reduce the overall cost of financing for developers.

India’s emergence as a green energy powerhouse

India has committed to achieving net-zero emissions by 2070, and green hydrogen will be a key enabling lever to achieve this aspiration. India’s potential domestic demand for green hydrogen (and its derivatives), coupled with rising demand in Asia, is enabling it to rapidly position itself as a major contender in the global green energy landscape as a low-cost producer and exporter of green hydrogen and ammonia.

India benefits from among the region’s lowest levelised cost of electricity due to its abundant renewable energy resources, combined with supportive policy. To date, India has already deployed over 192GW of renewable capacity5 and targets 500GW of non-fossil fuel electricity by 2030.6 With electricity accounting for 60% - 70% of green hydrogen production costs, the availability of this low-cost, scalable renewable energy is the cornerstone of cost competitiveness for the production of green molecules.

The country’s strong policy impetus has already catalysed significant private sector investment and project announcements. Major Indian developers are aggressively pursuing green hydrogen and ammonia projects.

Reliance Industries has unveiled ambitious plans to establish a fully integrated green hydrogen ecosystem, aiming for 100GW of renewable energy by 2030 to produce green hydrogen at some of the world’s lowest costs. Adani Group has announced plans for an integrated green hydrogen project with an initial capacity of 1Mtpa, expanding to 3Mtpa, supported by substantial renewable energy generation.

ACME Group is developing large-scale green ammonia facilities, including a project in Oman aiming to leverage India’s expertise and supply chain, with significant portions of offtake potentially directed towards Asian markets. NTPC, India’s largest power utility, is also actively pursuing green hydrogen production, including a pilot project for green methanol synthesis and hydrogen blending in natural gas pipelines.

These multibillion-dollar commitments underline the industry’s confidence in India’s potential and the NGHM's enabling framework. The first ever green ammonia auction by the Solar Energy Corporation of India delivered a price of Rs55.75 /kg (US$641/tonne) for green ammonia supply to Paradeep Phosphates covering 75,000 tonnes per annum over ten years. This marks a dramatic fall from the previous benchmark of Rs100+/kg (US$1000+/tonne) from global auctions, and even competes favourably with grey ammonia at US$515/tonne.

The drop in production costs is a structural game-changer, lowering the levelised cost of ammonia and strengthening India’s export narrative, particularly given the high cost of renewables in land-scarce and resource-poor industrialised countries such as Japan and South Korea.

Regional collaboration and piloting are key to scaling a decarbonised Indo-Pacific

Ecosystem collaboration is essential to build on this momentum. Coordinated action among governments, industry, and financiers is vital to build infrastructure, harmonise standards, and develop bankable projects. DBS Bank has been playing a catalytic role in this transition – partnering with public and private stakeholders to shape innovative financing models, support project development, and help green molecules move from concept to mainstream reality.

Piloting low-carbon alternatives and emerging low-carbon technologies and infrastructure will be critical to decarbonising the toughest parts of the transition. The path forward lies in piloting pragmatic, replicable models. Starting off with a few bankable, demonstrable projects will lay the groundwork for regional collaboration, shape the regulatory framework and prove viability of attracting capital while building investor confidence for scaling. Each success refines frameworks, reduces risk and accelerates deployment.

The momentum is building. What is needed now is collective will, and decisive action, to turn these green corridors from pilots into pathways powering a decarbonised Indo-Pacific.