By Navin Sregantan & Gwendoline Tan

![]()

If you've only got a minute:

- It is important to control your spending before it spirals out of control.

- There are 3 main types of debt repayment programmes in Singapore – the Debt Consolidation Plan, Debt Management Plan, and Debt Repayment Scheme.

- They aim to help borrowers avoid bankruptcy or to be more disciplined in repaying debts.

![]()

Contrary to popular belief, big spenders and those who are careless with their money are not the only ones who risk racking up large debts.

Some people make small, frequent purchases (on credit) and do not think too much about it given their small ticket size. These small debts, if unattended, can easily add up and snowball over time, leaving them in the same predicament.

While the reasons that people accumulate debts can vary, the common underlying thread is their inability to manage their debts and repayments before it spirals out of control.

Read more: Rolling over credit card debt is no game

Debt repayment programmes

If you find yourself in this situation, there is light at the end of the tunnel. There are 3 main debt repayment programmes in Singapore that can help borrowers to avoid bankruptcy, or exercise greater discipline in the repayment of their outstanding debts.

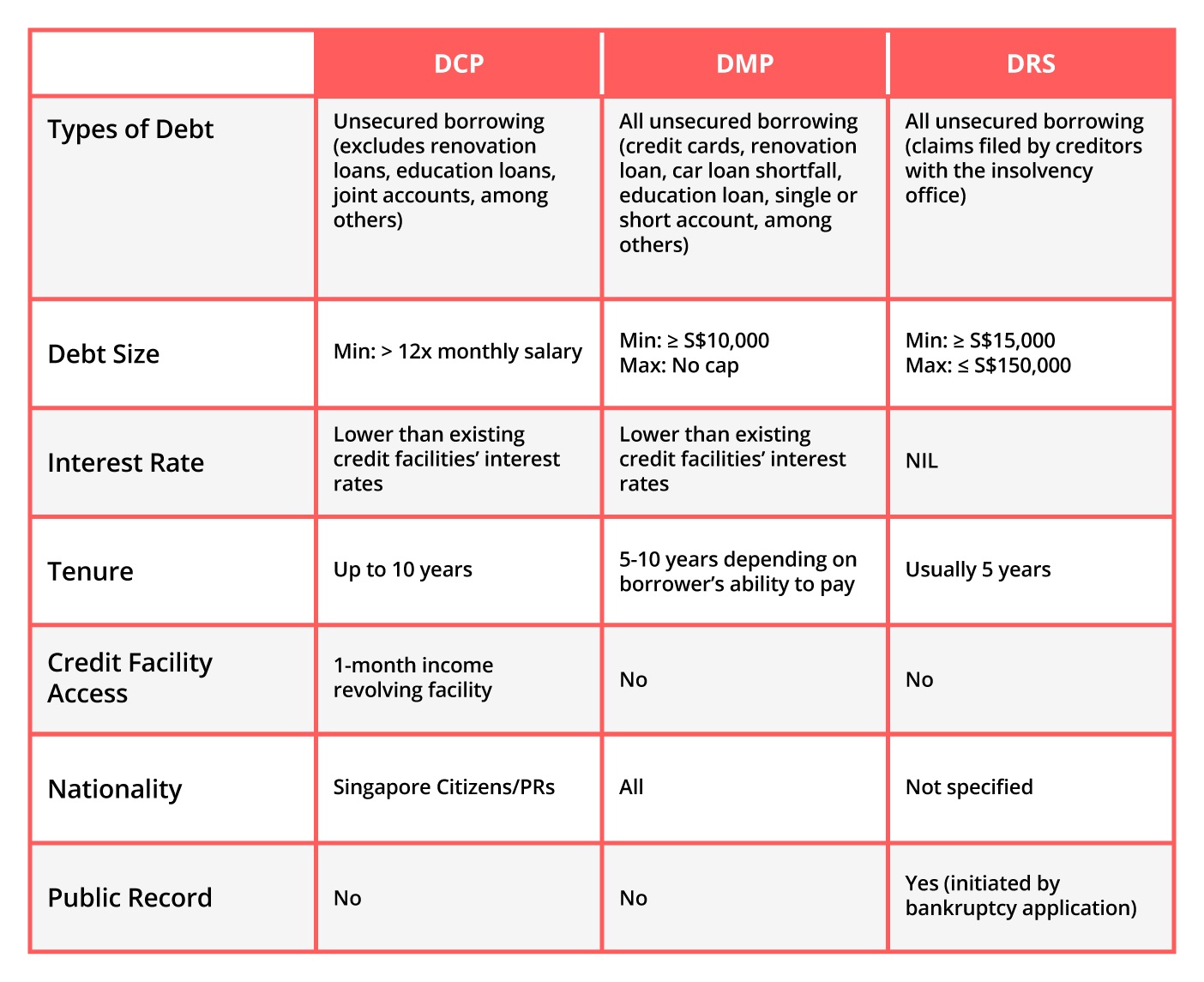

1. Debt Consolidation Plan

A Debt Consolidation Plan (DCP), as its name suggests, offers you the option to consolidate your unsecured debts (like credit cards or other types of unsecured loans) with 1 of the participating financial institutions in Singapore, like DBS.

Simply put, this means that if you take up a DCP with DBS, your debts will be combined and then paid off by DBS. In return, you will have to commit to paying off DBS through making regular payments – often at a lower interest rate – across a pre-agreed period of time.

For example, while interest rates for credit cards range between 20 and 26% per annum (p.a.), a DCP with DBS allows you to consolidate and pay off your debts at an interest rate of 3.58% p.a. (EIR of 6.56% p.a.*).

Among other requirements, your total outstanding unsecured debts with financial institutions in Singapore must exceed 12 times of your monthly income before you can qualify to apply for a DCP.

Since the DCP is aimed at helping you cut debt, you will not be able to apply for any additional unsecured loans from another financial institution unless your outstanding unsecured debt has first been reduced to 8 times your monthly income or less.

The DBS DCP comes with a DBS Visa Platinum credit card with a limit of up to 1x your monthly income and no annual fee, meaning that you do not have to worry about managing your daily essentials.

*Effective Interest Rate – based on S$63,000 loan amount for 96-months loan tenure and inclusive of processing fee. The interest rate offered to you is based on your personal credit profile and may differ from the published rate and the rate offered to other borrowers, subject to the bank’s discretion.

Read more: Ease your financial burden with a DCP

Find out more about: DBS Debt Consolidation Plan

2. Debt Management Programme

The Debt Management Programme (DMP) is offered by Credit Counselling Singapore (CCS), a registered charity and an agency that assists individuals who face unsecured debt problems. It is a formal arrangement facilitated by CCS with major local consumer banks and credit card issuers.

Similar to the DCP, the DMP allows you to make monthly repayments of your unsecured consumer debts – such as credit cards and overdraft – to creditors over a reasonable period of time. However, while the DCP consolidates your debts under 1 financial institution, the DMP does not. The monthly repayments will be made to each creditor directly, until the outstanding debts are fully paid off.

To determine if you can qualify for the DMP, CCS conducts a 1-hour debt advisory session with eligible applicants to understand and work out your financial commitments and outstanding debt. Where possible, they will work out a payment proposal that could include an extended repayment period, or moderated interest rates, for creditors to approve.

Upon successful application to be placed on a DMP, your monthly instalments will be within your servicing capacity, You are expected to make prompt, full, and regular payments during the repayment term.

3. Debt Repayment Scheme

The Debt Repayment Scheme (DRS) is administered by the Official Assignee (OA) from the Ministry of Law’s Insolvency Office. Unlike the DCP or DMP, it is not application-based.

If you make a bankruptcy application to the High Court of Singapore (for amounts of debt under S$150,000), the court may refer you to the OA. The OA will then assess your eligibility and suitability for the DRS.

If deemed eligible, the OA will then assist you in drawing up a DRS, after which you must then begin paying off your debts through the OA within an agreed period of up to 5 years.

With the DRS, you can avoid bankruptcy and the restrictions that come with declaring as a bankrupt.

Read more: DRS – A lifeline to avoid bankruptcy

Find out more about: Ministry of Law Singapore, Information for Debtors

How do they compare?

Live within your means

No matter what your financial circumstances are, the bottom line is this: Live within your means.

To do this, you need to have a good grasp of your current financial situation, have enough emergency funds set aside, and manage your monthly inflows and outflows well.

Be careful of racking up debt, especially with the ease of access to credit cards and personal loans. If you do take up debt, ensure that you make it priority to pay it off in a timely manner to avoid it snowballing out of control.

And at the end of the day, if you find yourself struggling with debt, consider one of the 3 debt repayment programmes to help ease your situation.

Read more: Habits to embrace in your financial journey

Ready to start?

Check out digibank to analyse your real-time financial health. The best part is, it’s fuss-free – we automatically work out your money flows and provide money tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.