7 financial ratios to gauge your financial health

![]()

If you’ve only got a minute:

- Financial ratios aren’t limited to businesses and stocks. They can also be used to evaluate your financial health.

- Personal finance ratios can help determine your money strengths and weaknesses, identify potential pitfalls and help you make informed financial decisions for the long-term.

- Find out how these ratios can help you understand areas concerning your liquidity, debt management, savings, investments, and solvency better.

![]()

Financial ratios form an integral part of a company’s financial statement and are often useful in guiding investors in their investment decisions. However, these ratios aren’t limited to businesses and stocks.

In similar fashion, you (and I!) can utilise specific ratios to evaluate your financial health. Unlike corporate ratios, personal financial ratios are relatively easy to compute and can be used to determine your money strengths and concurrently, shed light to areas that require improvement.

Here are 7 noteworthy ratios you could use to help you identify potential financial pitfalls and make informed financial decisions for the long haul.

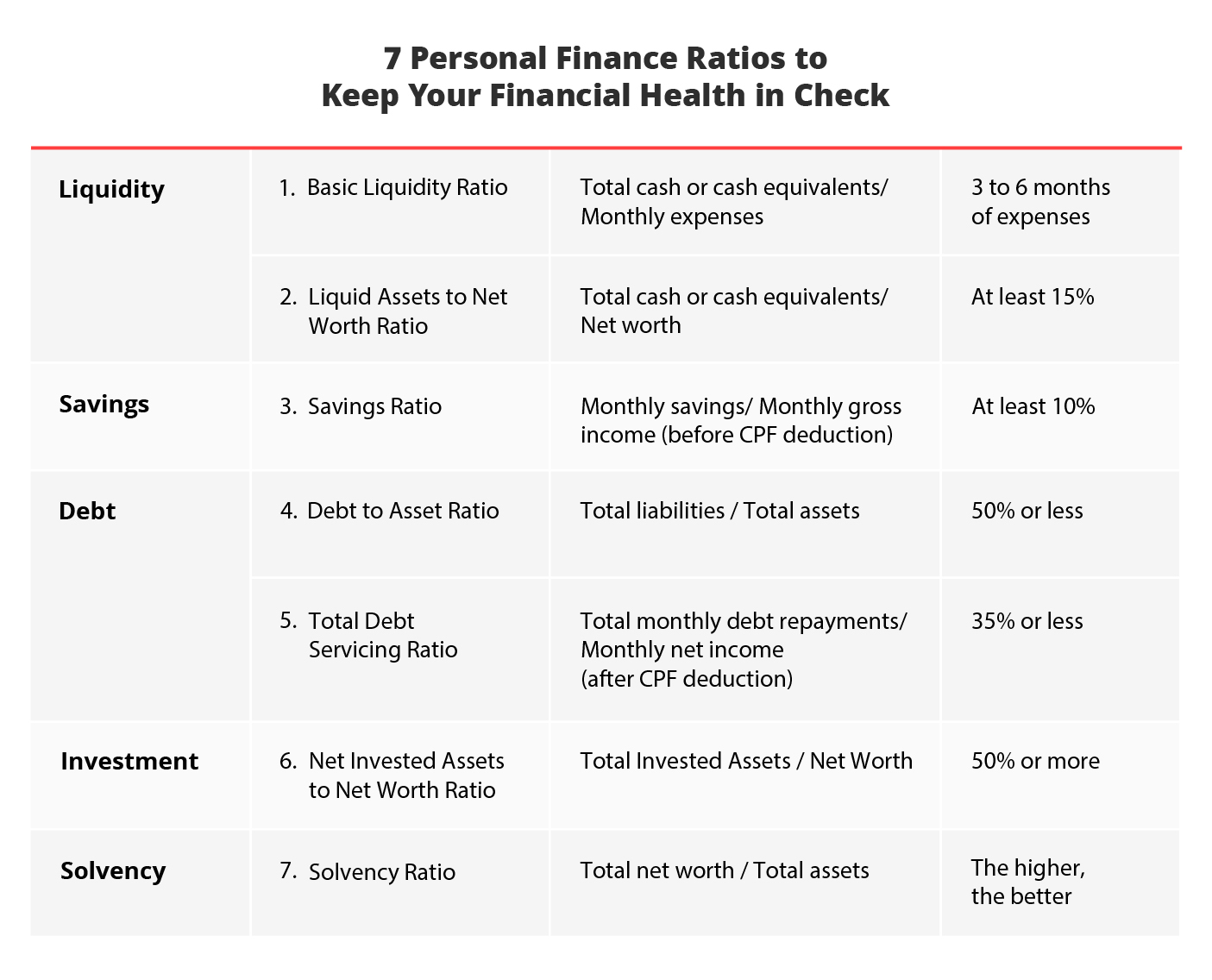

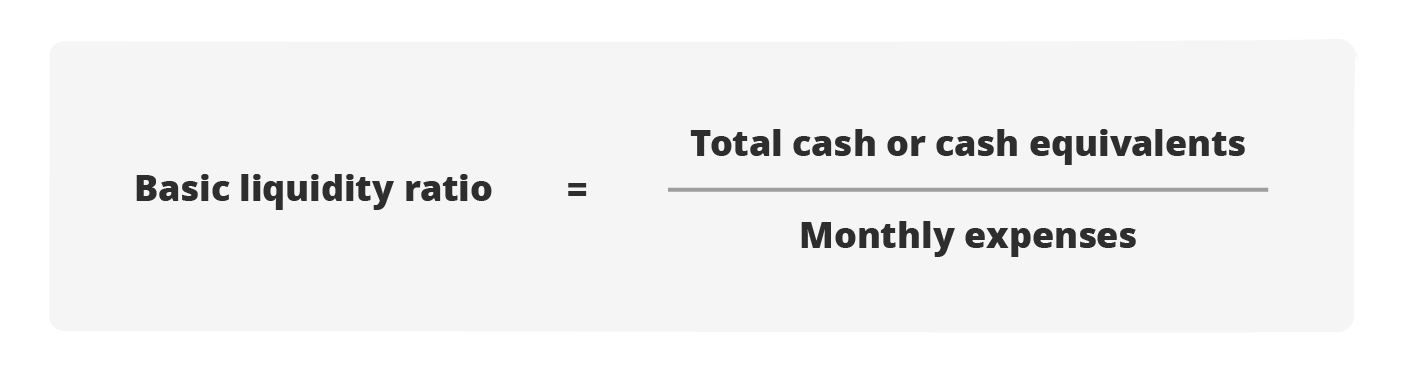

1. Basic liquidity ratio

Also known as the emergency fund ratio, the basic liquidity ratio alerts you to whether you have adequate cash reserves to cover your monthly expenses in the event of an emergency, such as job loss (retrenchment) or unexpected expenses (urgent medical bills). It also specifies the number of months you can continue paying your expenses should you lose your income source.

Monetary assets are the most liquid since they can be converted quickly to cash with no loss in value. These include your cash or cash-equivalent securities like fixed deposits and Singapore Savings Bonds (SSBs).

The ratio is derived by comparing your total cash (or cash equivalents) to your monthly expenses. The higher the number, the more liquid your assets.

As a guide, it is recommended to set aside at least 3 to 6 months’ worth of expenses. If you are self-employed or have a higher number of dependants, you may want to consider increasing your liquidity ratio to 12 months instead.

2. Liquid assets to net worth ratio

Your net worth is the value of your total assets (individually-owned: property, investments, cash) less all your liabilities (common debts: mortgage, car loan, personal loan, etc).

This ratio measures the percentage of your total assets that are cash (or cash equivalents). The higher the liquidity ratio, the bigger the buffer you have against any unexpected income loss.

While it is good to have contingency cash for a rainy day, avoid having a high liquidity ratio as this would mean you’re keeping too much cash on hand and not enough in investments.

A good rule of thumb is to have at least 15% of your net worth in cash or assets that can be readily converted into cash to cover short-term debt obligations or other emergency situations where you might require cash quickly.

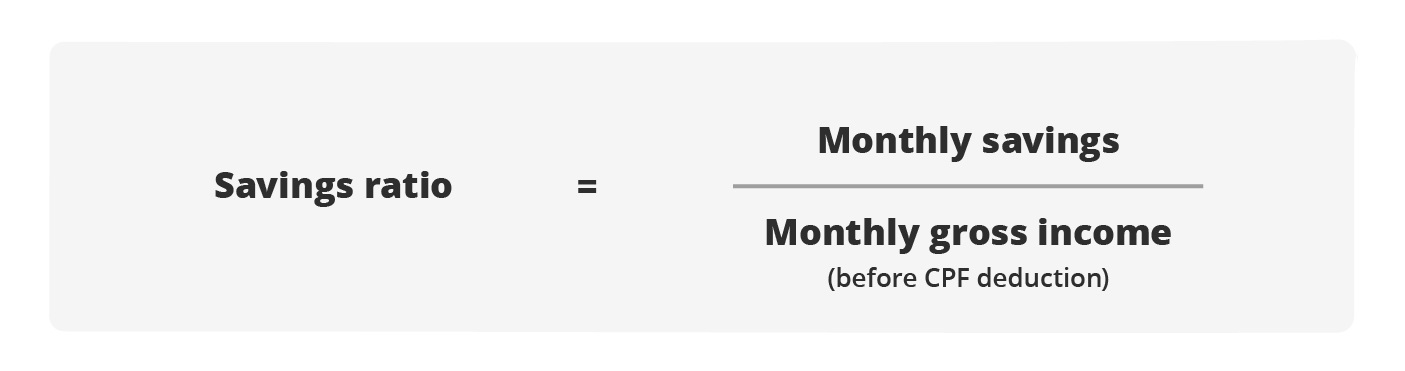

3. Savings ratio

How much of your monthly income that you channel towards savings is determined by this ratio. The higher the ratio, the better, as this reflects your ability to save more than you spend. However, do note that having too much idle cash is not prudent because we need to work our money harder to mitigate against inflation and longevity risks.

You should try to save at least 10% of your income and this savings ratio should be one that you are comfortable with.

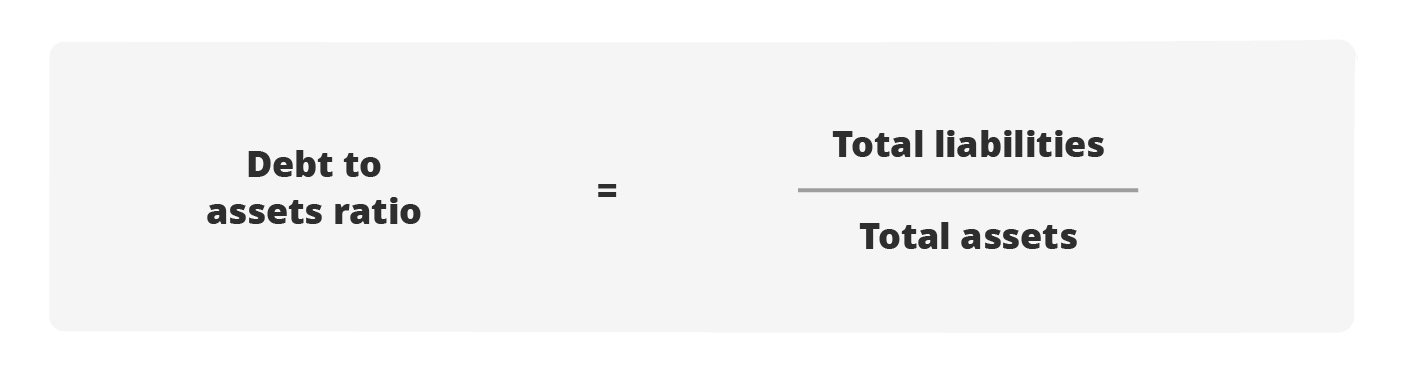

4. Debt to assets ratio

This ratio indicates how much of your assets are funded by debt and helps you understand if you have borrowed more than you should. The higher your debt ratio, the higher your liabilities and this could potentially lead to solvency issues.

For example, if you have recently made a big-ticket purchase such as a house and have an ongoing mortgage, you should probably refrain from taking out another loan for a brand-new sports car as this would increase your liabilities. Unless you are certain you have not borrowed beyond your repayment capacity and can afford to pay back the loan, it is best to wait till you settle outstanding debts first.

As a guide, you should work towards a ratio of less than 50%.

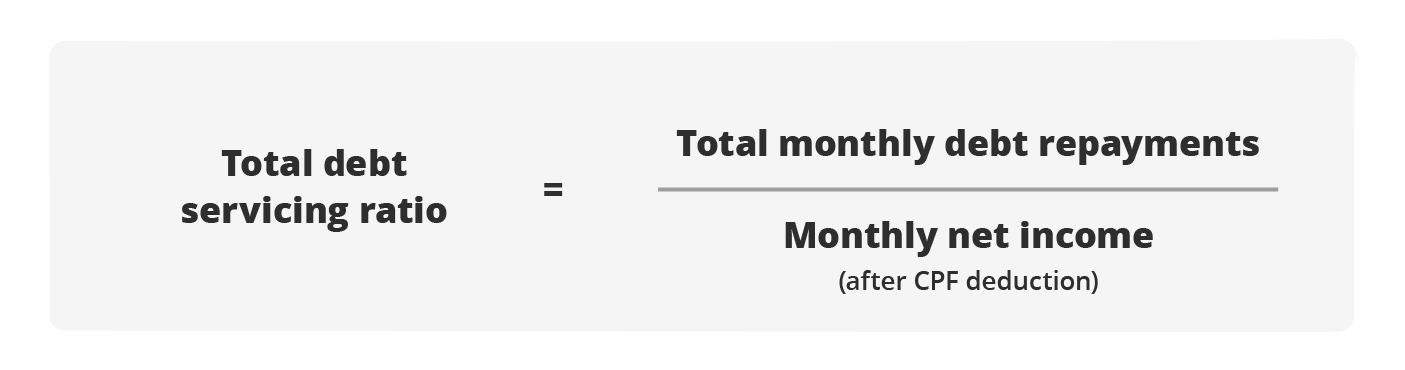

5. Total debt servicing ratio (TDSR)

This ratio calculates the amount of your salary that is used for your regular debt settlements.

Ideally, a ratio of 35% or below means you have ample income to fulfil your monthly debt repayments.

Let’s assume John’s monthly net income is $5,000 and he services a $1,500 mortgage and $1,000 car loan repayment monthly. The remaining amount constitutes his savings, investments, and other expenditure.

2,500/5,000 x 100 = 50%

It is best for John to start reducing his debts to derive a ratio of 35% or less, to ensure higher savings and less debts. He can consider reducing his monthly debts by 1) purchasing a lower-priced car (or sell his car and take public transport), 2) opt for a longer home loan tenure to increase his liquidity by refinancing or repricing. Following the Monetary Authority of Singapore’s (MAS) guideline for home loans, the total debt servicing ratio (TDSR) should not exceed 55%.

The mortgage servicing ratio (MSR) – applicable to HDBs and ECs, and TDSR – applicable to both public and private properties - are home loan limits implemented by MAS to prevent overleveraging. Simply put, it is to prevent people from taking up huge home loans that exceeds their affordability and to address the lack of loan restrictions previously that could have led to property speculation.

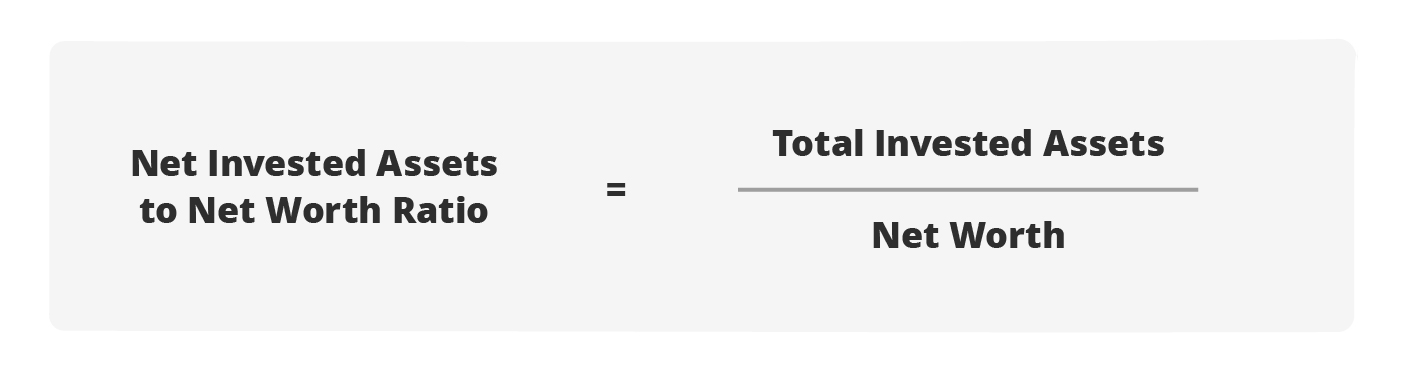

6. Net invested assets to net worth ratio

This ratio lets you know how much of your assets (excluding your home) are effectively used to accumulate wealth for you for the long-term. In short, it tells you how well you’re using your money to work harder for you.

Start channelling surplus cash into investments early and adopt a long-term investment horizon. The earlier you start investing, the higher the potential of wealth accumulation, thanks to the power of compounding. Due to a longer time horizon, you’ll also be able to ride out market volatility over time. Not only can you make your money work harder for you, investing protects you from the loss of purchasing power due to inflation as well.

To position yourself well for your retirement years, strive to have at least 50% of your assets invested.

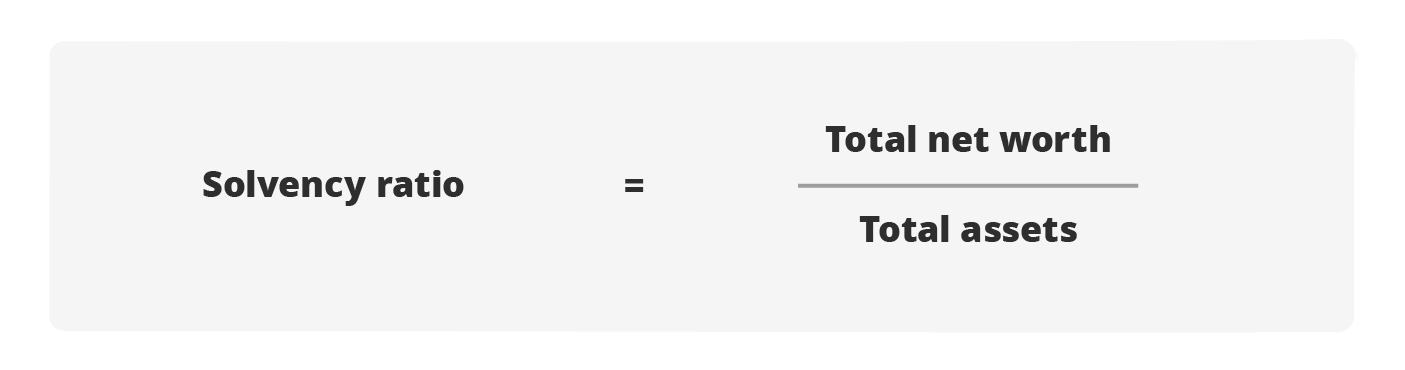

7. Solvency ratio

Finally, the solvency ratio offers clarity as to whether you have sufficient assets in your portfolio to service your debts. To calculate net worth, subtract your liabilities/debts from your assets. It lets you know the probability of becoming insolvent or bankrupt.

Sometimes, we acquire assets and use debt to finance them which may result in a higher amount of debt (loan) than the value of the asset (property). An example is when you take on a mortgage loan after buying your home.

The solvency ratio is calculated to gauge your risk of getting bankrupt due to the inability to settle the debts taken. As such, the higher the solvency ratio, the stronger your financial position.

In Summary

These 7 personal finance ratios can be used as a starting point to gauge your financial health and as a guide to enhance your finances. These ratios are in no way a substitute to a holistic financial plan.

Do check out the Plan & Invest tab on digibank to set up a budget, identify and close insurance and investing gaps and plan for your retirement.

Ready to start?

Check out digibank to analyse your real-time financial health. The best part is, it’s fuss-free – we automatically work out your money flows and provide money tips.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

All investments come with risks and you can lose money on your investment. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single product issuer.

Disclaimer for Investment and Life Insurance Products

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)