Low-risk ways to grow money with CPF

By Shawn Lee

![]()

If you’ve only got a minute:

- Achieve higher returns on your CPF Ordinary Account (OA) savings by transferring them to your Special Account (SA) if you are below age 55.

- Invest your CPF and Supplementary Retirement Scheme (SRS) savings for potentially higher returns.

- Optimise and grow your money by investing and topping up your CPF and learn more about Voluntary Housing Refund (VHR) scheme, Matched Retirement Savings Scheme (MRSS) and Supplementary Retirement Scheme (SRS).

![]()

Investing has long been recognised as an effective way to grow wealth. It is especially important in an inflationary environment to invest so that the value of our money is not eroded. Yet, many continue to have doubts on how to start or are simply fearful of the risks involved.

Despite these challenges, there are ways to optimise and grow our money with CPF and still stay on the safer side of things. Here are 6 steps you can take.

1. Topping up your CPF

Your CPF monies in your Ordinary Account (OA) attract a risk-free interest of 2.5% p.a. while your CPF Special Account (SA) balance grows at a rate of at least 4% p.a.

If you are below age 55, you can earn an additional 1% interest per annum on the first S$60,000 of your combined CPF balances, capped at S$20,000 from OA.

If you are 55 or older, you will receive an extra 2% interest per annum on the first S$30,000, and 1% per annum on the next S$30,000 of your combined CPF balances, also capped at S$20,000 for the OA portion.

The difference between your OA and SA may seem little but it is significant when compounded over time. Since the SA interest is higher, it makes sense to park your money there if you are below age 55 and have no immediate need for funds in your OA.

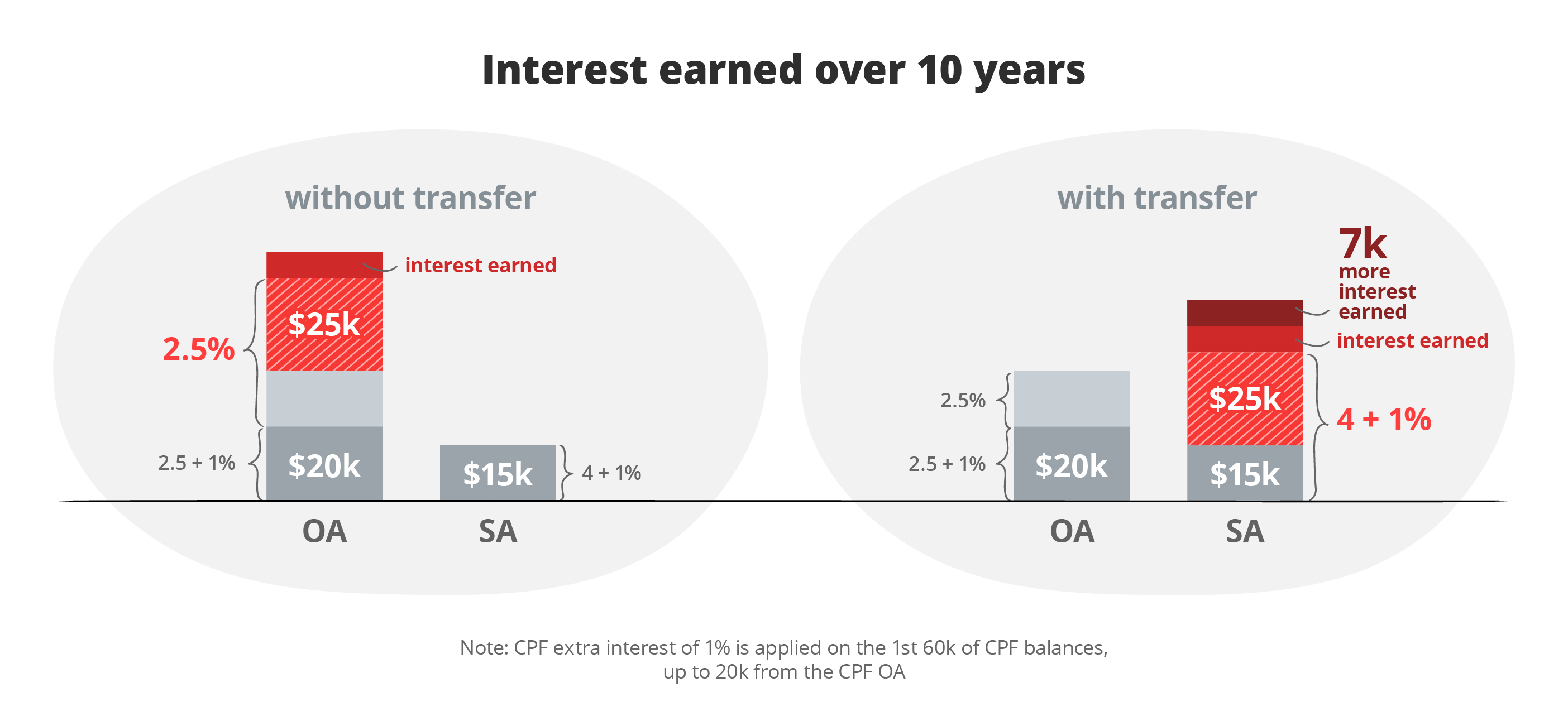

CPF transfer

One way to achieve higher returns on your OA is by transferring your OA savings to your SA if you are below age 55.

Here’s an example on the difference it will make

Prior to the transfer, do carefully assess your financial obligations because the transfer is irreversible. Unlike the savings in your OA, the funds in your SA cannot be utilised for housing or educational expenses. If you require the money in your OA to fund your home purchase or existing home loan repayments, this option may not be suitable for you.

Cash top-ups

Alternatively, if you have spare cash and sufficient liquidity, you can consider making cash top-ups to your CPF accounts to earn risk-free interest and build up your nest egg.

There are 2 types of top-ups you can make.

- Retirement Sum Topping-Up Scheme (RSTU)

The RSTU is meant to boost your CPF savings so that you will have higher monthly payouts under the Retirement Sum Scheme, or CPF LIFE once you reach your Payout Eligibility Age. You can top-up your SA - for those below age 55 - to the prevailing Full Retirement Sum (FRS) or your Retirement Account (RA) - for those age 55 and above to the prevailing Enhanced Retirement Sum (ERS).

Find out more: CPF LIFE or Retirement Sum Scheme?

- CPF Voluntary Contribution (VC)

While you may already be working and making mandatory monthly contributions to your CPF account, you can still boost your CPF savings with cash top-ups via the VC scheme – the “VC-3A” - to your 3 CPF accounts (Medisave Account (MA), OA and SA), subject to the CPF annual limit of S$37,740. These cash top-ups are particularly beneficial for self-employed persons or freelancers as an effective way to compound and grow their savings over time.

Both top-up methods are irreversible, and only cash top-ups under the RSTU can qualify for tax relief.

Read more: 6 ways to optimise your CPF for retirement

2. Voluntary Housing Refund (VHR)

You may rely on your OA funds to finance housing expenses, such as the initial downpayment, stamp duties, legal fees as well as subsequent monthly home loan repayments.

If you decide to sell the house, you are required to refund the OA funds used for the property, along with the accrued interest of 2.5% p.a. This is the interest that you would have earned if the money had remained in your OA.

The VHR is a scheme that allows you to refund OA savings for housing in cash, even if you have no immediate plans to sell your home. Full or partial cash refunds can be made at any given point, up to the total principal amount that was withdrawn for the property plus the accrued interest. Refunding your OA can help you avoid a significant reduction in your sales proceeds in the future due to the substantial amount of accrued interest owed.

3. Matched Retirement Savings Scheme (MRSS)

If you’re looking to enhance your retirement savings, you may consider the MRSS. Eligible CPF members can take advantage of this scheme to receive a matching government grant for every dollar of cash top-ups, S$2,000 annually, with a lifetime cap of S$20,000 .

You are eligible if you’re aged 55 and above with RA savings below the current Basic Retirement Sum (BRS), draw a monthly salary of not more than S$4,000 and own no more than one property with an annual value of S$21,000 or less.

Cash top-ups which qualify for the MRSS do not qualify for tax relief. Tax relief is only applicable to non-matched cash top-ups, up to an annual limit of S$16,000.

4. Investing with CPF

Are you seeking to maximise the potential returns on your CPF monies and make them work harder? One option is to invest using your CPF savings. However, this only makes financial sense if you are confident of beating the guaranteed risk-free 2.5% p.a. (OA) and 4% p.a. (SA) interest provided by the CPF Board. For some, using CPF funds for investment purposes may present fewer psychological barriers than investing with cash savings, especially when liquidity is a concern.

CPF Investment Scheme (CPFIS)

The CPF Investment Scheme (CPFIS) consists of 2 separate schemes for the OA and SA savings, each with different requirements.

To be eligible, you must be at least 18 years old, not an undischarged bankrupt, and have an OA balance of minimally S$20,000 and/or SA balance with at least S$40,000. If you’re a new applicant, you are required to complete the CPFIS Self-Awareness Questionnaire (SAQ) to assess your suitability for investing under CPFIS.

Generally, OA offers more flexibility in terms of investment product choices, while SA has stricter limitations. For example, you can invest in shares, gold, bonds, mutual funds, real estate investment trusts (REITs), higher-risk ETFs and higher-risk unit trusts under CPFIS-OA. For CPFIS-SA, you will only be able to invest in less-risky products such as T-bills, Singapore Government bonds (SGS), endowment policies, annuities and lower-risk unit trusts and Investment Linked Policies (ILPs).

Read more: Investing with CPF and SRS

Should you invest your CPF funds?

The OA typically earns a lower interest rate compared to other investment options. By investing in higher-return assets, such as stocks or bonds, you can potentially achieve better long-term growth, outpace inflation, and preserve the value of your CPF monies.

However, do bear in mind investing involves market fluctuations and the possibility of incurring losses and you may risk having to liquidate your investments during a market downturn should you require urgent access to your CPF funds. It is thus important to only invest your savings if you do not foresee using them in the near future.

Read more: Do more with your CPF

5. Supplementary Retirement Scheme (SRS)

The SRS is a voluntary savings scheme that offers tax savings and complements your CPF savings for retirement. You can contribute any amount, as many times as you wish throughout the year to a cap of S$15,300 for Singaporeans and Permanent Residents (PRs), and S$35,700 for foreigners.

Every dollar you contribute to your SRS account is eligible for tax relief (subject to a yearly total relief cap of S$80,000). This helps to reduce your taxable income and maximise tax savings.

It’s worth noting that leaving your contributions in your SRS account only earns 0.05% p.a., comparable to rates offered by banks for savings accounts. Consider investing your SRS monies to potentially reap higher returns. For those who are risk-averse, they can consider safer instruments like fixed deposits, insurance plans, T-bills, Singapore Savings Bonds and short duration investment grade bond funds.

Find out more: Why and where to invest your SRS savings

Carefully assess your personal financial circumstances to ensure that your SRS contributions are savings that you can commit to for the long term. This is because there is a 5% withdrawal penalty if you start withdrawals before the penalty-free withdrawal period.

6. Grow your money to beat inflation and longevity risks

It is important to safeguard the value of our money and not let it idle in a plain vanilla savings account. With increasing life expectancy and medical advancement, the chances of us outliving our savings are greater too. To mitigate these risks, it is essential to pursue certain investing strategies to make our money work harder so as to achieve financial security in the long term.

There are many ways to grow your money and it does not always require investing in high-risk products. Start maximising the growth of your CPF monies and surplus savings today. Meanwhile, continue to empower yourself with financial knowledge so that your confidence in the area of investing will be enhanced over time and you can make informed decisions and take on more investing risks if necessary and when you are ready.

Ready to start?

Start planning for retirement by viewing your cashflow projection on Plan tab in digibank. See your finances 10, 20 and even 40 years ahead to see what gaps and opportunities you need to work on.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)