Redefining retirement – 7 considerations

By Lorna Tan

![]()

If you’ve only got a minute:

- Realistically, the “real” golden years – characterised by a good mix of health and wealth - would mostly come before the official retirement age of 63.

- Is it worth being stuck in a job you don’t enjoy? By managing your risks better and with proper money management, you can enhance your quality of life.

- The demise of the traditional 3 life stage means there is more flexibility in how we want to pursue our interests throughout life without being shackled to specific timeframes to finish formal education and a fixed career path.

![]()

Much has been written about the importance of retirement planning and how to grow our wealth and assets via saving and investing. The objective is to accumulate a nest egg – comprising cash, assets, and passive income streams - to fund our needs and wants in our golden years.

However, certain retirement norms that worked for past generations may not work for us. With a longer lifespan, traditional thinking revolving around retirement has also evolved.

Here are 7 retirement considerations.

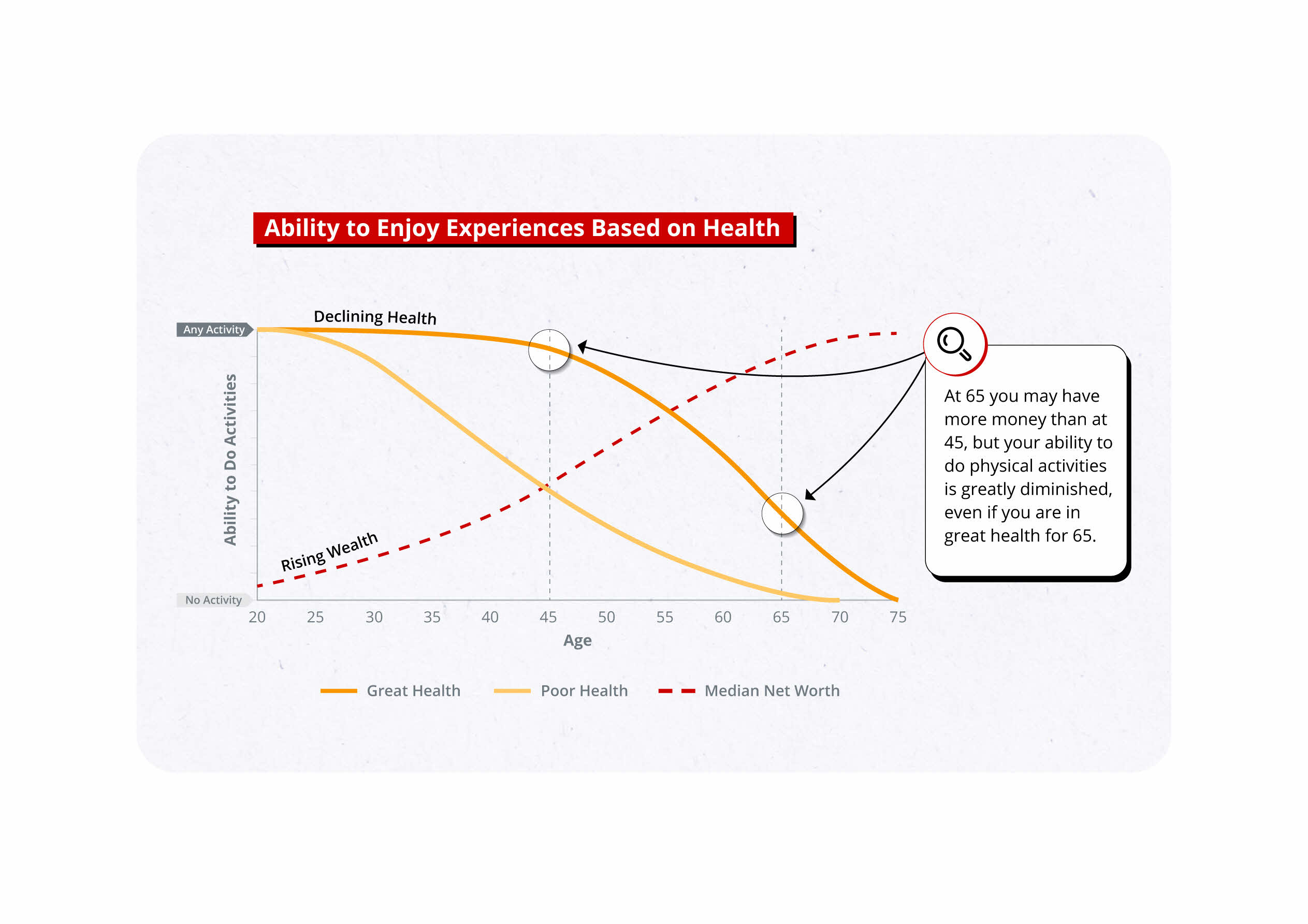

1. Balancing health, time, and money

To get the most out of life, the 3 basics we need to have are health, time and money. But for most people, these 3 seldom come together. When we are younger, most of us would have good health, more free time but less money.

If we consider our golden years as the period from age 65 - when we can start receiving our CPF LIFE monthly payouts - most of us will have time and money but may suffer from declining health. Of course, how healthy we are differ from person to person.

2. Re-defining golden years

It is no wonder that author Bill Perkins suggests in his book Die With Zero, that sometime between the 2 extremes is where the “real” golden years lie. Realistically, the “real” golden years would mostly come before the official retirement age of 63.

If we consider our golden years as the period of maximum potential enjoyment because it includes a good mix of health and wealth, then these would be the years when we should be spending on what we value or bring us happiness, instead of delaying gratification and hoarding our assets. When we re-define when our golden years are, it will signal the period that we should utilise our money to optimise fulfilment and create more precious moments.

Source:"Die With Zero" by Bill Perkins

This means that for those who have planned well, they ought to start spending their wealth down much earlier than what is traditionally recommended. If they wait till they’re in their mid-60s to dip into the nest egg, they may end up working longer than necessary, and for money they may never get to spend, added Perkins.

It doesn’t mean that they need to stop working before the official retirement age but they can start spending more than they earn.

3. Leaving a bequest

Asian societies tend to place a priority on the tradition of passing down family heirlooms and bequests for their loved ones. Perhaps this explains why some CPF members prefer to opt for the CPF LIFE Basic Plan, as they have the misconception that it will definitely offer a bigger bequest amount to their loved ones, relative to the other 2 CPF LIFE plans.

On the contrary, there will be no bequest available under the 3 CPF LIFE Plans after the member hits about age 90. So, if you are going to live past 90, the Basic Plan may be a poor choice as the monthly payouts are lower than that of the Standard Plan, and there is zero bequest.

When it comes to selecting a suitable CPF LIFE plan, consider your own needs first – that is, how much monthly payouts you require - above anything else.

I fully agree with a friend who said that questioning the purpose of leaving a bequest and what’s the best way to show love to our children, does not equate to a prescription for living a hedonistic life.

More thought can be given over the purpose of leaving a bequest and what might end up being an unintended bequest. The latter happens if we die prematurely and leave a higher bequest than what was initially intended.

Sure, we all love our children, but is giving them money the best way to show our love? Is giving them money when we die (which likely means our children would be about age 60 and quite settled in life by then) the best way to do it?

For those who can afford to help their children after setting aside resources for a comfortable retirement, it may make more sense to help their children financially now – especially with the higher cost of living and their higher financial needs - when they really need help. The same can be said about giving to charity while you are still around, instead of leaving it as a bequest.

4. How much is enough?

There is also the question of how much is enough for a sustainable retirement.

Are we working because we need the money, enjoy our work or simply because we are on autopilot and have become addicted to our job? Perhaps the thrill of making our first million has resulted in a bigger desire to make more? Over time, we allow ourselves to be robbed of actually living our life. The opportunities to build memories with our loved ones when we were busy making money are lost forever. We will never be young again, and neither will our parents, children, relatives, and friends.

The top 20% of the population can consider how much wealth they should accumulate and how they grow it. For instance, is it worth being stuck in a job they don’t enjoy? By managing their risks better and with proper money management, they can enhance their quality of life.

For the middle 60%, rather than scrimping and living anxiously about running out of savings, consider investing wisely in a diversified portfolio that is aligned with their life goals, financial situation, and risk profile. The portfolio can comprise equities, fixed income and insurance like annuities and retirement insurance plans, to provide income streams to fund their retirement lifestyle.

In addition, a sound estate plan will come in handy if mental incapacity occurs, as well as for proper distribution of assets upon death. Doing so will help to minimise leakage from their estate.

5. Demise of traditional 3 life stages

Coupled with longevity and inflation, the traditional 3 life stages of education, work and leisure is losing its relevance. This has many implications on how the government and employers perceive the ageing population as well as on education opportunities and employment policies. Some employers are friendlier to older staff and there is even one that is offering lifelong employment as long as the staff remains relevant.

We need a framework where age does not matter and what matters are interest, capability, and aptitude. For example, the SkillsFuture programme is not biased against age and encourages continuous learning.

For individuals, it presents more flexibility in how we want to pursue our interests throughout life without being shackled to specific timeframes to finish formal education and a fixed career path.

With a comprehensive financial plan to help navigate our life journey, we can afford to hit the pause button in life to smell the roses and come back refreshed to embark on a new venture, if we so desire.

6. Trend of “unretired”

Studies have shown that if you enjoy your job and will miss the social network and identity it offers, your health may suffer after retirement. While this applies to professionals whose jobs are mainly bound up with self-esteem and identity, it is also true for non-professionals.

Increasingly, there are people who have officially retired but have decided to re-join the workforce and become “unretired”. Reasons are financial and psychological such as the need for routine and mental stimulation and company.

So, focus on getting the most from your longer lifespan by continuing to learn and work. You can stay in work that is aligned with your life purpose and this need not be the same job nor require the same number of work hours, that you had in your younger years.

7. Health is wealth

In our efforts to achieve a sustainable financial future, some of us neglect what’s equally important, if not more important - our health. We know we are living longer lives than our grandparents, but it would be more fulfilling if we are living better and healthier lives for the long run.

After all, it is not enough to have money alone. We can make more good use of and be able to enjoy our wealth only if we have good health. As such, measuring our years in good health is key. Doing so requires effort and a good understanding of how exercise and diet can translate to more good years.

So, have a multi-prong approach to retire well by re-defining your golden years, empower yourself with financial knowledge, inculcate the discipline to exercise and eat well, and understand what gives you purpose in your life.

Ready to start?

Start planning for retirement by viewing your cashflow projection on Plan tab in digibank. See your finances 10, 20 and even 40 years ahead to see what gaps and opportunities you need to work on.

Speak to the Wealth Planning Manager today for a financial health check and how you can better plan your finances.

Disclaimers and Important Notice

This article is meant for information only and should not be relied upon as financial advice. Before making any decision to buy, sell or hold any investment or insurance product, you should seek advice from a financial adviser regarding its suitability.

That's great to hear. Anything you'd like to add? (Optional)

We’re sorry to hear that. How can we do better? (Optional)