India

India is emerging economies in the world and its government is putting a focus on foreign investment and pursuing pro-international trade policies to enhance economic growth.

A relatively low-cost region in which to operate with a skilled workforce, India can be utilised as a strategic and operational support centre for wider operations. India is a major exporter of information technology (IT) services, particularly in business process outsourcing and software services, which is the fastest growing part of the economy

The Indian government has been instituting an ongoing series of economic reforms to increase the efficiency of doing business within the global economy and to overcome the market's historical limitations, particularly in relation to foreign direct investment (FDI). These changes have included the privatisation of state-owned enterprises, a reduction of financial controls, industrial deregulation and an increase in FDI caps.

Corporate Treasury in India

India is one of the fastest-growing emerging economies in the world, and a global leader in IT. In this section, we highlight some of the key factors relevant to treasury and cash management in India.

Financial Market Development

● Mumbai is ranked 65th in the 2021 Global Financial Centres Index produced by Z/Yen Group, 30 places lower than in 2020.br /> ● The Indian rupee (INR) is convertible for current accounts but not capital accounts. The Reserve Bank of India (RBI) has imposed capital controls in the past, such as in August 2013, when it cut overseas remittances by individuals to USD75,000 from USD200,000, and reduced overseas investments by Indian companies by three-quarters.

● India has a skilled, cost-effective English-speaking workforce, a strong rule of law and a pro-business government. The digital business infrastructure, such as telecommunications and payment systems, is also of a high standard.

Sophistication of Banking Systems

● Historically, India’s banking sector has been heavily influenced by its state-owned banks, however, a list of the sector’s largest banks now includes both public and private institutions. There are more than 100 banks in India, including over 40 foreign banks.

● Daily foreign exchange turnover in India accounted for 0.5% of global turnover in the Bank for International Settlements’ latest Central Bank Survey.

● India's bond market is not well-developed and remains small compared with developed economies. While it is composed of both corporate and government bonds, government bonds dominate and are the most liquid component of the bond market. Total corporate bond issuances outstanding stands at more than IRD33 trillion.

● India is a member of the Asian Clearing Union.

Regulatory Bodies

● The banking system in India is regulated by the Reserve Bank of India (RBI). Regulation is in line with international standards. RBI approval is required in certain cases for the repatriation of funds.

Tax

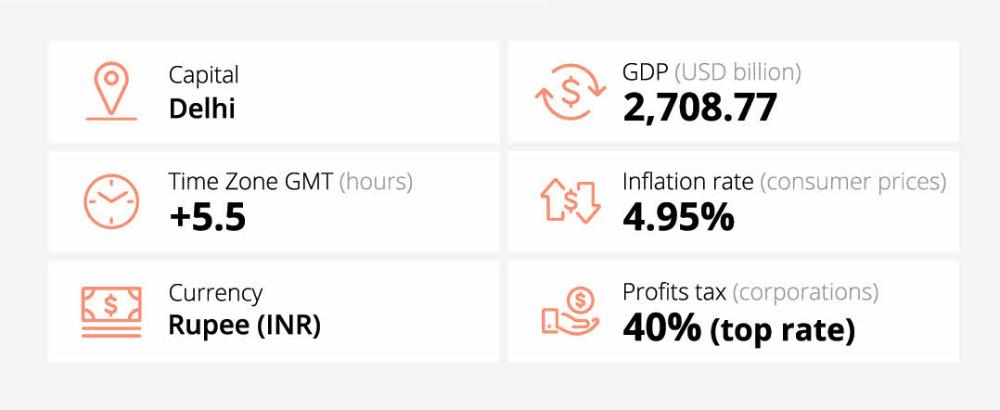

● The corporate income tax rate is 30% for resident companies. Companies with an income of more than INR10 million pay a surcharge of 10%. A “health and education cess” or levy of between 2% and 4% is also charged.

● Foreign companies pay corporate income tax of 40%, with a surcharge of 10% if total taxable income exceeds INR10 million, as well as a health and education cess of 4%.

● A reduced corporate income tax (CIT) rate of 22%, plus a 10% surcharge and 4% health and education cess, is available to existing domestic companies that meet certain conditions. Newly established domestic manufacturing companies and firms involved with electricity generation may qualify for a beneficial CIT rate of 15%, plus a 10% surcharge and 4% health and education cess.

● In certain circumstances, companies may be liable for a 15% minimum alternative tax plus a 10% surcharge and 4% health and education cess if their tax liability under the Income-tax Act is not more than 15% of their book profits

● Resident companies are taxed on their worldwide income. Foreign companies are taxed on income that is received or generated in India.

● Foreign companies are considered to be resident in India if they have a Place of Effective Management in India.

● There is no branch profits remittance tax on remittance of profits by the branches of foreign companies to their head offices.

● Interest income received by a foreign company is subject to a withholding tax of 20% plus surcharge and cess. Under certain circumstance, the withholding tax rate on the interest will be reduced to 5% plus surcharge and cess.

● Interest expenses that are used for business purposes are generally tax deductible, unless the interest is paid to related parties, in which case the expense is restricted to 30% of earnings before interest, taxes, depreciation and amortisation. There are no thin capitalisation rules in India.

● The dividend distribution tax has been abolished for dividends distributed after April 1, 2020.

● A securities transaction tax of between 0.001% and 0.125% is charged depending on the nature of the securities.

● Capital gains tax is charged at 10%, 15% or 20% depending on the type of asset and whether the gains are long term or short term.

● Tax incentives are available to certain industries operating in Special Economic Zones (SEZs). For example, offshore banks and international financial services centres that meet certain conditions are eligible for a 100% tax exemption on specified income for five years and a 50% concession for a further five years.

● Goods and services tax (GST) is charged at 5% to 28% depending on the nature of the goods or services involved and the individual state. There are also special rates and GST compensation cess on certain goods. The export of goods and services is zero-rated.Additional details can be found here: https://cbic-gst.gov.in/gst-goods-services-rates.html

● Resident companies are charged withholding tax of 10% on interest. Foreign companies pay withholding tax of 20% on interest and 20% on dividends if no treaty is in place. Where a tax treaty is in place, withholding tax on interest ranges from 5% to 15%, and withholding tax on dividends ranges from 5% to 25%.

● India has tax treaties with more than 90 countries and territories.

● India is a signatory to the Organisation for Economic Co-operation and Development’s Multilateral Competent Authority Agreement,through which information is exchanged between tax administrations, to provide a single, global picture on some key indicators of economic activity within multinational enterprises.

Benefits for Local Treasury

● The RBI is broadening the country’s derivative and debt markets.

● A number of Indian banks are part of the Society for Worldwide Interbank Financial Telecommunication’s (SWIFT) global payments innovation initiative, improving cross-border payment infrastructure.

● India is a relatively low-cost region in which to operate and has an adequately skilled workforce, enabling companies to use it as a strategic and operational support centre for wider operations.

● Resident and non-resident companies are permitted to participate in cross-border sweep structures, but for non-resident companies, foreign-exchange control rules and withholding tax on inter-company loans apply.

● Cash concentration is available, but non-residents may have to pay withholding tax on interest.Notional pooling is not permitted in India.

Banking

Bank Accounts

● Residents are permitted to open INR accounts domestically. Foreign currency accounts both in India and overseas are subjected to certain conditions prescribed by the RBI.

● Non-residents (as defined under Foreign Exchange Management Act, 1999) can open INR account in India, subject to conditions prescribed by the RBI.

Legal and Regulatory

● The RBI's Board for Financial Supervision oversees India’s banking sector, with the National Bank for Agriculture and Rural Development overseeing provincial rural and most cooperative banks under the auspices of the RBI. The RBI also implements foreign currency controls.

● A resident company must be registered under the Companies Act 2013 and rules made there under.

● A company incorporated outside India can enter Indian markets as a Wholly Owned Subsidiary in India or as a Joint Venture Partner of an Indian Company. A company incorporated outside India can also set up a branch, project office or liaison office in India under various regulations.

● India has anti-money laundering legislation in place and is a member of the Asia/Pacific Group on Money Laundering (APG), the Eurasian Group on Combating Money Laundering and Financing of Terrorism (EAG) and the Financial Action Task Force (FATF). It also operates the Financial Intelligence Unit under the Ministry of Finance, which is tasked with safeguarding the financial system from the abuses of money laundering, terrorism financing and other economic offences.

Payments

Payment Systems

| UPI (Unified Payments Interface) |

| |

| NG–RTGS | India’s national real-time gross settlement (RTGS) system |

|

| CTS | Cheque Truncation System |

|

| NACH | National Automated Clearing Services |

|

| NEFT | National Electronic Funds Transfer |

|

| BBPS | Bharat Bill Payment System |

|

| IMPS (Immediate Payment Service) | Interbank Mobile Payments Service |

|

| AEPS (Aadhaar Enabled Payment System) |

|

Payment Instruments

Credit Transfers

● High-value (more than INR 200,000) and urgent credit transfers settled via NG–RTGS in approximate real time.

● Low-value, non-urgent, bulk credit transfers settled via NACH within the same day.

● One-to-one electronic payments settled via NACH or NEFT within the same day.

Direct Debits (auto debits)

● NACH Debit used for regular transfers for transactions up to INR 10,000,000 and supports both C2B and B2B Payments.

● Settled via NACH on T+0.

Card Payments

● Declining in popularity as digitised payments become more popular.

● Debit and credit cards were used for 20% and 12% of in-store purchases in 2020, respectively.

● Visa and MasterCard are the main brands of credit card used, and these are cleared the next day.

● RuPay is a domestic debit and credit card payment network used at ATMs, POS devices and e-commerce websites. It is operated by the NPCI.

● Most card credits and debits are processed by National Financial Switch (NFS) and settled via the Clearing Corporation of India (CCIL) within the same or the next day. Multi-application cards have been introduced by the RBI for use in banking, postal and financial services. The banks authorised to issue these cards are: ICICI Bank, HDFC Bank and Oriental Bank of Commerce.

Online Payments

● India’s fast adoption of financial technology (fintech) has mainly been attributed to the government’s aggressive demonetisation programme aimed at becoming a cashless society

● According to government agency Invest India, the country’s fintech sector is valued at $31 billion, as of November 2021, making it the third-largest fintech ecosystem globally.

● The government has provided initiatives such as the establishment of UPI and Aadhaar Enabled Payment System (AEPS), and an application programming interface (API) aimed at increasing efficiencies in payments and banking systems through the provision of a unique identification number for every Indian resident.

● The government has set up an eight-member steering committee to supervise the development of the fintech sector and formulate regulations that allow a more flexible environment and promote financial inclusion to ensure that every Indian has a bank account.

● Mobile wallet adoption in India is one of the highest in the world. One measurement of this is the increase in transactions using the UPI interface, which recorded a 15x jump in the three-year period up to May 2021, according to Invest India

Digital Currencies

● Despite government concerns and the lack of regulation, the country’s cryptocurrency investment market is growing. Government agencies, such as the Finance Ministry and RBI, are reportedly working towards a conceptual framework in which cryptocurrencies are regulated as an “asset” class. An announcement is expected by the next General Budget, February 2022.

Cash, Cheques and Money Orders

● Despite the demonetisation programme, cash has had a resurgence in popularity and was used in 34% of all in-store purchases in 2020, making it the most popular payment method.

● There’s been a significant drop in cheque usage as digitised payments become more popular.

● Cheques truncated and processed via CTS through grid system, which is divided into three grids.

● Money orders are a common service provided by India Post, which offers electronic (eMO), instant (iMO) and international (IFS) orders. Western Union and MoneyGram also operate in the country.

Foreign Exchange

India has been gradually relaxing its foreign exchange controls since 1991. Despite this policy, a number of restrictions still remain.

FX Landscape

● The official currency of India is the Indian rupee (INR) which is partially convertible. The INR is convertible for current accounts but not capital accounts.

● India’s monetary policy is set and managed by the Reserve Bank of India (RBI), which sets interest rates and governs foreign exchange controls.The RBI has imposed capital controls in the past.

● The exchange rate of the INR is determined by market supply and demand, however, the RBI will intervene in the market by buying or selling foreign currencies, either directly or through public sector banks, if deemed necessary.

● There are offshore INR centres in London, New York, Singapore and Dubai.

● Exchange-traded currency futures are available in India through the National Stock Exchange, the Bombay Stock Exchange and the Multi Commodity Exchange of India. The trading of currency futures is jointly regulated by the RBI and the Securities and Exchange Board of India.

FX Management

● Residents companies are permitted to open INR accounts domestically. Foreign currency accounts both in India and overseas can also be opened subjected to certain conditions set by the RBI.

● Non-residents (as defined under Foreign Exchange Management Act, 1999) can open INR accounts in India, subject to conditions set by the RBI.

● Indian companies are allowed to take out FX-denominated loans and bonds overseas subject to certain guidelines.

● India offers a wide range of products to help companies manage FX risk, including FX swap, FX spot, FX options, FX futures, and cross-currency options.

Exchange Controls

● Only banks and institutions licensed as authorised dealers by the RBI can deal in foreign exchange. FX accounts can only be opened with licensed institutions.

● Foreign investment in India is allowed in the majority of sectors, and for many sectors, non-resident companies do not require prior approval from the Government or the RBI. For certain industries, including telecoms and pharmaceuticals, the level of investment is capped, with regulatory approval required above these limits. Following a recent rule change, government approval is currently required for FDI from countries that share a border with India.

● Cross-border inward remittances into India are allowed under the Rupee Drawing Arrangement, capped at INR15 lakh (IND1.5 million) for trade-related transactions, but there are no other limits on remittance amounts or the number of remittances that can be made. Foreign exchange transactions in India are subject to goods and services tax at 18%.

● Profits made by foreign companies can be repatriated once all taxes have been paid, unless the company operates in the defence sector. Companies must submit an application for remittance to the RBI with supporting documents.

● Restrictions on trading FX futures were recently liberalised, allowing traders, institutional investors and eligible foreign investors to trade currency futures and options contracts involving INR with positions of up to USD 1 billion, or 15% of the total open interest, whichever is higher.

Trade

India’s trade with the rest of the world has expanded rapidly in the past decade as the government pursues pro-international trade policies. Its largest export partners are the United States (US), China and the United Arab Emirates (UAE), in terms of exports in US dollars, according to Trading Economies.

Trading Landscape

● Member of the South Asian Free Trade Area.

● Approximately 270 free trade zones, special economic zones and warehousing zones, which offer duty free imports and full or partial exemptions from certain taxes, such as income tax and goods and services tax. Many of the zones are specific to certain products or industries.

● Member of the World Trade Organisation since January 1995.

● No autonomous sanctions regime, however, it does implement some United Nations (UN) sanctions, including sanctions against individuals and entities suspected of having terrorist links as named by the Unites Nations Security Council.

Import Regulations

● Importers must obtain a permanent account number (PAN) from the Income Tax Department and an Importer-Exporter Code (IEC) number from the Directorate General of Foreign Trade

● For authorisation to import, companies must obtain a Registration Cum Membership Certificate (RCMC) from the relevant authority or commodity board.

● Most goods are classed as freely importable items and do not require an import licence. Import licences are required to import goods classed as ‘restricted’, such as precious stones, chemicals, pharmaceuticals and animal products. Licences are issued by the Director General of Foreign Trade and are valid for 24 months for capital goods and 18 months for raw materials. Some goods, such as petroleum products, are classified as canalised items and can only be imported through specified channels or government agencies.

● India has a complex system of customs duty made up of different components. Imported goods are subject to goods and services tax, known as integrated goods and service tax, and compensation cess if applicable. A basic customs duty (BCD), which varies according to the product and country of origin is also levied, along with a social welfare surcharge of up to 10% on the BCD. The Indian Trade Portal includes a search function to enable importers to establish what rate of BCD they will pay: https://www.indiantradeportal.in

Export Regulations

● Exporters must obtain a permanent account number (PAN) from the Income Tax Department and an Importer-Exporter Code (IEC) number from the Directorate General of Foreign Trade, which acts as an export licence.

● For authorisation to export, companies must obtain a Registration Cum Membership Certificate (RCMC) from the relevant Export Promotion Council, Federation of Indian Export Organisations, authority or commodity board.

● Exported goods are zero-rated for GST. Customs duty is levied on only a limited number of exported goods.

● A range of options are available, including letters of credit, export factoring, export credit and forfaiting. Export insurance is available through the Export Credit Guarantee Corporation.

● Export contracts and invoices must be denominated in a freely convertible currency or Indian rupees. Export proceeds should be realised in a freely convertible currency, except for exports to Iran. Export proceeds must be realised within nine months.

Sources (Intro & Corporate Treasury)

World Economic Forum, BIS, PwC, KPMG, Trading Economies, CIA World Factbook, IMF, World Bank, Reserve Bank of India

Sources (Banking & Payments Sources)

India Brand Equity Foundation, J.P. Morgan, National Payments Corporation of India, Financial Express, The Fintech Times, EcommerceDB, DataReportal.

Sources (Foreign Exchange)

The Reserve Bank of India, Bank for International Settlements, the Economic Times, Securities and Exchange Board of India, PwC, Ministry of Commerce and Industry, Government of India

Sources (Trade)

Ministry of Commerce and Industry, Government of India, Trading Economics, the Indian Trade Portal, Department of Commerce of the United States Government, PwC

This Market Profile is brought to you by DBS. Get in touch with us for further insights on doing treasury in India and take advantage of our innovative solutions to empower your business. Click here to find out more.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?