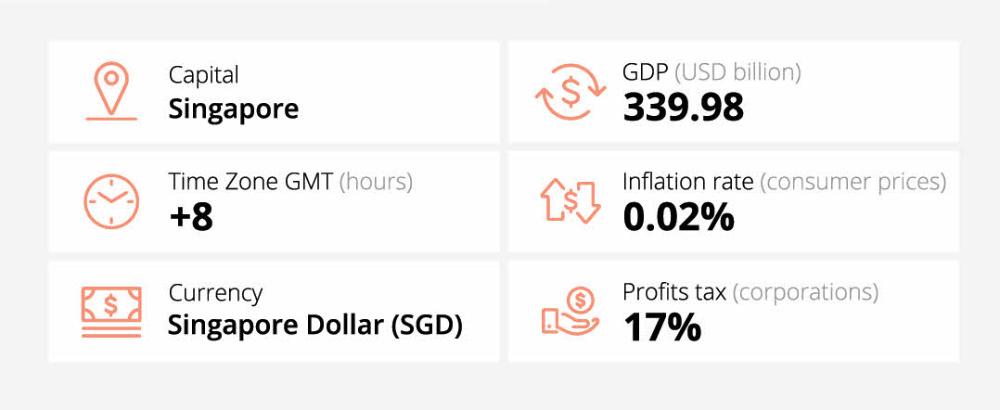

Singapore

Singapore, a vibrant city-state in the heart of Southeast Asia, offers businesses a number of competitive advantages in setting up a treasury function. Singapore is rated as the most competitive economy in the world, according to the Global Competitiveness Index 2019.

The city has a well-established business infrastructure with a transparent and efficient institutional framework, a pool of highly skilled English-speaking professionals and a regulatory system that meets international standards. Singapore is also the largest foreign exchange market in Asia Pacific and more than 200 banks have a presence in the country, with a growing number choosing it as a base for their regional operational headquarters. Singapore also has an established financial sector, mature capital markets and a wide variety of sophisticated financial instruments.

Singapore has preferential investment and business policies with members of the Association of Southeast Asian Nations (ASEAN). In total it has 14 bilateral FTAs, and 11 regional FTAs. Singapore also has tax treaties with 88 countries and territories, offering tax incentives for businesses. In

addition, it offers approved finance and treasury centres a reduced corporate tax rate of 8% on income derived from qualifying finance and treasury centre (FTC) services.

With 5G trials underway, the government is rolling out programmes to help industries adopt and utilise 5G technology. These include training programmes, innovation labs and start-up collaborations. In 2020, the Monetary Authority of Singapore (MAS) launched a SG125 million support package for financial and financial technology (fintech) sectors as they deal with the challenges of COVID-19. This fund is on top of a host of other government initiatives, such as innovation grants, a regulatory sandbox, the API Exchange, and Project Ubin, to assist the country’s growing fintech sector.

Singapore's geographic location has made it a major shipping and logistics hub, and it is the second busiest port in the world and the top maritime capital.

Corporate Treasury in Singapore

Singapore offers a number of competitive advantages for setting up a treasury function. Here, we highlight some of the key factors relevant to treasury and cash management.

Financial Market Development

● Singapore is ranked fifth in the latest version of the 2021 Global Financial Centres Index published by Z/Yen Partners.

● Singapore has a well-established business infrastructure with a transparent and efficient institutional framework, a pool of highly skilled English-speaking professionals and international regulatory standards

● The Monetary Authority of Singapore (MAS) has set up a FinTech and Innovation Group to oversee regulatory policies and development strategies in the financial sector, and support private enterprise.

● There are no restrictions on capital flows in and out of Singapore.

Sophistication of Banking Systems

● There are around 200 banks in Singapore, including 40 representative offices, with a growing number choosing it as a base for their regional operational headquarters.

● Singapore is the banking hub of Southeast Asia.

● Singapore is the largest foreign-exchange market in Asia Pacific and the third largest in the world (Bank for International Settlements triennial global survey 2016).

● Singapore's debt market has grown in depth and breadth over the past decade, with an extensive range of both Singapore government securities and foreign corporate bonds available, with outstanding local currency bonds worth USD380.4 billion at the end of 2020.

Regulatory Bodies

● MAS regulates the banking industry with a regulatory framework in line with international standards. MAS is revising the capital requirements for Singapore-incorporated banks to align them with the Basel III minimum requirements from January 1, 2023.

Tax

● The corporate income tax rate is 17%. There is a partial tax exemption of 75% on the first SGD10,000 and 50% on the next SGD190,000. For the 2020 year of assessment, there was a rebate of 25% of the corporate income tax payable, subject to a cap of SGD15,000.

● Both resident and non-resident companies are taxed on their Singapore-sourced income. However, in respect of resident companies, foreign-sourced income is taxed when it is remitted to Singapore, although a remittance exemption may be available subject to the fulfilment of certain conditions.

● Foreign company branch profits are taxed at the same rate as resident company profits. There is no branch profits remittance tax on the remittance of profits to a head office by the branch of a foreign company.

● According to Budget 2022, the standard rate for GST will be increased to 9% – 7% to 8% with effect from 1 January 2023; and 8% to 9% with effect from 1 January 2024. The export of goods and international services are zero-rated, and some goods and services are exempted from GST, including financial services. GST is generally not charged on the import of services, although from 1 January 2020 a reverse-charge has been introduced on local businesses that make exempt supplies, and those that do not make any taxable supplies. Overseas providers that make significant supplies of digital services to customers in Singapore are also required to register for GST in Singapore.

● Income from investment such as dividends, interest and rent is subject to tax in Singapore, although Singapore dividends are tax exempt.

● Gains made on capital transactions are not subject to tax in Singapore unless it can be proven that the gains were trade in nature.

● Interest expenses that are used for business purposes are generally tax deductible.There are no thin capitalisation rules in Singapore.

● Stamp duty of 0.2% is charged on the purchase price or value of shares, whichever is higher.

● Withholding tax of 15% is charged on interest paid or payable to non-resident companies where no tax treaty is in place. Rates range from 0% to 15% where a tax treaty is in place and the non-resident can provide a Certificate of Residence. Certain domestic law exceptions are available.

● Under the Financial Sector Incentive scheme (FSI), certain activities for qualifying institutions are taxed at 5%, while a broader range of financial activities are taxed at 13.5%.li>

● Income derived from qualifying finance and treasury centre (FTC) services is taxed at 8%. Interest payments to overseas banks or approved network companies, where the funds borrowed are used for approved qualifying FTC services, are exempt from withholding tax.

● Various tax incentives, including exemptions and concessionary rates on qualifying income, are available for companies that set up regional or international headquarters in Singapore.

● Singapore has tax treaties with 93 countries and territories.

● Singapore is a signatory to the Organisation for Economic Co-operation and Development's Multilateral Competent Authority Agreement, through which information is exchanged between tax administrations, to provide a single, global picture on some key indicators of economic activity within multinational enterprises.

Benefits for Regional Treasury Centres (RTCs)

● Singapore offers approved FTCs a reduced corporate tax rate of 8% on income derived from qualifying FTC services.

● Singapore offers approved FTCs withholding tax exemptions on interest payments on loans from overseas banks or approved network companies provided the funds borrowed are used for qualifying FTC services.

● Singapore is the regional risk management and treasury hub for Asia Pacific, as well as a renminbi gateway, second to Hong Kong in the region.

● Singapore has preferential investment and business policies with ASEAN members and a total of 14 bilateral FTAs, and 11 regional FTAs.

● Singapore's Global Trader Programme provides a reduced corporate tax rate of 5% or 10% on qualifying income, including from physical trading, brokering of physical trades and derivative trading income, for three or five years.

● Cash concentration is widely available in Singapore on a domestic and cross-border basis. Different legal entities can participate in the same cash-concentration structure.

● Notional pooling is allowed in Singapore on both a domestic and cross-border basis. Different legal entities can participate in the same notional cash pooling structure.

Comparison of Singapore and Hong Kong as a Location for RTCs

● Corporate income tax for approved treasury operations in the two locations is broadly similar, at 8% for Singapore and 8.25% for Hong Kong.

● Singapore offers a withholding tax exemption to FTCs on interest payments on funds borrowed from non-resident banks and approved network companies, provided the funds are used for qualifying FTC services, while Hong Kong has no withholding tax on interest.

● Singapore has the edge in terms of tax treaties, having agreements with more than 90 locations, compared with around 40 for Hong Kong.

● Both cities have highly developed infrastructure, deep capital markets and strong talent pools.

● Singapore tends to be preferred by businesses that are active in Southeast Asia, while Hong Kong tends to be the location of choice for corporations focused on Mainland China due to its status as an offshore renminbi hub and its location within the Greater Bay Area development.

Banking

Bank Accounts

● A company with a permanent or registered address in Singapore and with its management operations in Singapore is regarded as resident.

● Residents, both domestic and overseas, and non-residents may hold foreign exchange and local currency (SGD) accounts. Local currency accounts are freely convertible into foreign currency for residents and non-residents.

● Residents and non-residents have overdraft facilities available to them.

● Interest is available to demand deposit and currency accounts.

Legal and Regulatory

● MAS takes on the role of central bank and operates autonomously. It does not require full central bank reporting.

● Singapore is a member of the Association of Southeast Asian Nations (ASEAN) and Asia-Pacific Economic Corporation (APEC).

● Singapore has in place anti-money laundering legislation which is applied by MAS. It is also a member of the Financial Action Task Force.

● (FATF), Asia/Pacific Group of Money Laundering (APG) and Group of International Finance Centre Supervisors (GIFCS).

● A financial intelligence reporting unit has been set up, the Suspicious Transaction Reporting Office (STRO), which is a member of the Egmont Group.

Payments

Payment Systems

| FAST (Fast And Secure Transfers) | Interbank electronic transfer system |

|

| PayNow | Digital funds transfer system |

|

| MEPS+ | Singapore's Real Time Gross Settlement (RTGS) system |

|

| ACH (Automated Clearing House) | Nationwide clearing system |

|

| IBG (Interbank Giro System) | Deferred multilateral net settlement system |

|

| SGDCTS (SGD Cheque Truncation System) | Cheque and paper-based truncation system |

|

| USDCTS (USD Cheque Truncation System) | USD cheque- and -paper-based truncation system |

|

| NETS (Network for Electronic Transfers) | Interbank electronic credit and debit transfer system |

|

Payment Instruments

Credit Transfers

● Used for salary and supplier payments in SGD.

● High-value and urgent interbank transfers settled via MEPS+ within the same day.

● Low-value, non-urgent and high-volume electronic credit transfers settled via IBG within the same day.

● Paper-based payments used for standing orders and sometimes payroll payments.

Direct Debits (auto debits)

● Used for low-value, regular payments in SGD such as utility bills.

● Processed through IBG, for next day.

Card Payments

● Singapore has a high penetration of credit and debit cards, and their popularity has in turn boosted the widespread usage of contactless payment systems.

● Visa is main card of choice, with MasterCard and American Express also in use.

● Processed via NETS within the same day.

● Consumer payment options are diversifying as tech companies partner with financial institutions to offer key fobs and other wearable devices that incorporate tap-and-go technology.

● Stored-value cards come in two types: Single-purpose stored-value cards (SPSVC) used to pay only for services provided by the card issuer; and multipurpose stored-value cards (MPSVC) used for a variety of payments, with CashCard, ez-link and NETS FlashPay the most common. E-money payments are settled next day.

Online Payments

● The Singapore Quick Response Code (SGQR) combines multiple electronic payment schemes into a single SGQR code, simplifying mobile payments for both consumers and merchants and providing an ‘infrastructure-light’ payment solution. Co-owned by MAS and the Infocomm Media Development Authority (IMDA), SGQR was the first of its kind in the world and uses a series of protocols adapted from the specifications set out by EMVCo, the organisation responsible for setting global standards in debt and credit payments.

● The three leading global digital wallets — Samsung Pay, Apple Pay and Android Pay — have an established presence, with a network of local and regional mobile wallet providers, such as Dash, PayLah! and Alipay, infiltrating the digital payment market.

● PayLah! is operated by DBS/POSB, but can be used by non-DBS/POSB account holders. It has mobile payment and banking solutions, is operable using QR codes and has linked up with the 7-Eleven store network as a payment provider.

● DBS has launched the POSB digibank Virtual Assistant, a banking facility that operates through a ‘chatbot’, using Facebook Messenger as the media platform, and offering banking services beyond customer service.

Digital Currencies

● While cryptocurrencies are not legal tender, exchanges and trading are. The Inland Revenue Authority (IRAS) has set out GST requirements for digital payment tokens, such as Bitcoins and Ether.

● Singapore has become a hub for initial coin offerings (ICOs), and the government has provided a conducive environment for their use and exchange.

● One such example is the DBS Digital Exchange which offers investors a fundraising platform through offerings of security tokens and secondary trading of digital assets, including cryptocurrencies.

Cash, Cheques and Money Orders

● Cheques are the most common cashless payment method in terms of value.

● Truncated and cleared at ACH.

● Possible to use USD- and SGD-denominated cheques.

● USD and SGD cheques processed via SCHA and settled via MEPS+.

● While cash is also preferred, especially for low-value transactions, the government has stated its aim to reduce the use of cash and become cheque-free by 2025.

● • Money transfers (formerly known as money orders ) are available in Singapore through vendors such as Western Union and MoneyGram. Money can be sent domestically or internationally, either online or in person.

Foreign Exchange

FX Landscape

● The official currency of Singapore is the Singapore dollar which is fully convertible domestically and offshore.

● Singapore’s monetary policy is set and managed by regulator the Monetary Authority of Singapore, which sets interest rates.

● The exchange rate of the Singapore dollar is set against a basket of the currencies of Singapore’s main trading partners and rivals. It is managed by MAS and allowed to fluctuate within a policy band.

● Singapore is the third largest FX centre globally after London and New York, and the largest in Asia Pacific, according to the Bank for International Settlements Triennial Central Bank Survey.

● Singapore has average daily trading volumes of USD633 billion of FX and OTC derivatives, according to BIS.

● Singapore has a deep and liquid market for trading and hedging G10 currencies, as well as those for emerging Asian markets.

● Singapore is the region’s second biggest offshore renminbi centre after Hong Kong.

● More than 30 foreign exchange futures and options contracts are traded on Singapore-based exchanges.

● MAS is working with banks and trading platforms to build up Singapore’s e-trading infrastructure as it aims to position the city as the global FX price discovery and liquidity centre in the Asian time zone.

FX Management

● Resident companies can have accounts denominated in both local and a wide range of foreign currencies both onshore and offshore.

● Non-resident companies may also hold accounts in both local and foreign currencies. All accounts can be converted into other currencies.

● Companies are not required to convert their foreign currency receipts into SGD.

● Both resident and non-resident companies can borrow in all currencies, however, foreign firms that borrow SGD locally must use the money for productive activities to discourage borrowing for speculative purposes.

● Non-resident financial institutions can only borrow up to SGD 5 million in local currency, companies wishing to borrow more than this sum for use offshore must convert the excess funds into a foreign currency.

● Singapore offers a wide range of products to help companies manage FX risk, including FX options, FX spot and FX forward, FX time option forward, par forward, cross currency swap, and non-deliverable forward

Exchange Controls

● There are no restrictions on forward foreign exchange markets, but leveraged foreign exchange trading, including in OTC derivatives, is regulated by MAS and financial institutions conducting this activity must apply for a Capital Markets Services license.

● There are no restrictions on capital flows in and out of Singapore. No prior approval is required for inward investment or outward payments.

● There are no restrictions on the remittance of profits or dividends in any currency to other countries. No withholding tax is charged on dividends.

● Domestic and cross-border intercompany lending is allowed subject to transfer pricing rules.

● Foreign currency invoices must be converted into SGD using an approved exchange rate for goods and services tax purposes.

Trade

Singapore has an open economy that is driven by trade in goods and services. It is a member of the ASEAN Trade in Goods Agreement and its largest trading partners are China, Malaysia, and the United State

Trading Landscape

● Singapore has nine free trade zones.

The country’s Networked Trade Platform enables trade and customs matters to be managed online.

● Singapore’s biggest imports in 2020 were machinery and transport equipment, chemicals and chemical products and miscellaneous manufactured articles.

● Singapore has launched a digital cross-border trade platform with China, OneSME, to help local SMEs expand into each other’s markets.

● Singapore implements the United Nations Security Council (UNSC) sanctions, which prohibits the import, export and transhipment through Singapore of certain goods, as well as prohibiting companies from engaging in certain transactions with UNSC sanctioned countries.

● Singapore also has its own sanctions under the Terrorism (Suppression of Financing) Act, which covers sanctions against individuals and terrorist organisations. The Monetary Authority of Singapore also has its own regulations covering financial institutions.

Import Regulations

● All goods imported into Singapore are regulated under the Customs Act, the Goods and Services Tax (GST) Act and the Regulation of Imports and Exports Act.

● Importers are required to obtain a customs permit. This is also used to account for tax payments on goods. In certain circumstances, a short-payment permit is also required.

● Imported goods are subject to Goods and Services Tax (GST) of the cost, insurance and freight value. GST and duty are charged on intoxicating liquors, tobacco products, motor vehicles and petroleum products.

● GST and duty are suspended for goods imported to a free trade zone and are only payable when the goods are consumed within the free trade zone or leave the free trade zone. GST is also not paid on goods stored in zero-GST warehouses until they are removed from the warehouses.

● A range of financing options are available including letters of credit, bankers’ guarantees, import documentary collections and pre-shipment/post-shipment trade loans.

● The Singapore Customs Electronic Banker’s Guarantee (eBG) Programme was recently implemented to make the lodgement of banker’s guarantees more efficient.

Export Regulations

● All goods exported from Singapore are regulated under the Customs Act, the Regulation of Imports and Exports Act and the Strategic Goods (Control) Act.

● A customs export permit is required to export goods from Singapore. Goods are categorised as containerised cargo or conventional cargo.

● The following documents are required for exports and must be kept for at least five years from the date of permit application approval: customs export permit, invoice, bill of lading or airway bill, certificate of origin.

● GST and duty are not levied on exports from Singapore.

● A range of financing options are available including letters of credit confirmation, export documentary collections, export financing under letters of credit and invoice financing/factoring.

Sources (Intro & Corporate Treasury)

The World Economic Forum, The Monetary Authority of Singapore, PwC, Trading Economics, IMF, CEIC, CIA World Factbook, BIS, Enterprises Singapore, Asian Development Bank, Z/Yen Partners, Singapore Marine and Port Authority, Singapore Economic Development Board

Sources (Intro & Corporate Treasury)

The World Economic Forum, The Monetary Authority of Singapore, PwC, Trading Economics, IMF, CEIC, CIA World Factbook, BIS, Enterprises Singapore, Asian Development Bank, Z/Yen Partners, Singapore Marine and Port Authority, Singapore Economic Development Board Sources (Banking & Payments) The Association of Banks in Singapore, Infocomm Media Development Authority (IMDA), The Monetary Authority of Singapore, Singapore Business Review, DBS, SkillsFuture Singapore, The Government of Singapore (various ministries)

Sources (Foreign Exchange)

The Monetary Authority of Singapore, Bank for International Settlements, Baker McKenzie, Deloitte, PwC

Sources (Trade)

Ministry of Trade and Industry Singapore, Enterprise Singapore, Department of Statistics Singapore, Singapore Customs

This Market Profile is brought to you by DBS. Get in touch with us for further insights on doing treasury in Singapore and take advantage of our innovative solutions to empower your business. Click here to find out more.

That's great to hear. Anything you'd like to add?

We're sorry to hear that. How can we do better?